Get access to the same vehicle valuation tool that dealers rely on. With Black Book, you’ll have insider data to accurately assess trade-in and purchase values—empowering you to negotiate the best possible deal.

As summer 2024 approaches, more drivers are wondering if now is a good time to buy a used car. When it comes to the used car market, the details matter. With the average listing price hovering around $25,540, nearly unchanged from the start of the year, it might seem tough to get a deal. But the price is only half the battle, as you’re about to see.

Let’s dive into the details.

Three Crucial Considerations for Used Car Buyers: Credit Score, Budget, and Timeline

1. The Importance of Credit Scores in 2024

Does Credit Score Matter in 2024?YES. Knowing your current credit score will help you plan for the cost of financing. Planning to pay cash? GREAT! But if not, lenders will use your credit score and debt-to-income ratio to determine if you qualify for a car loan.

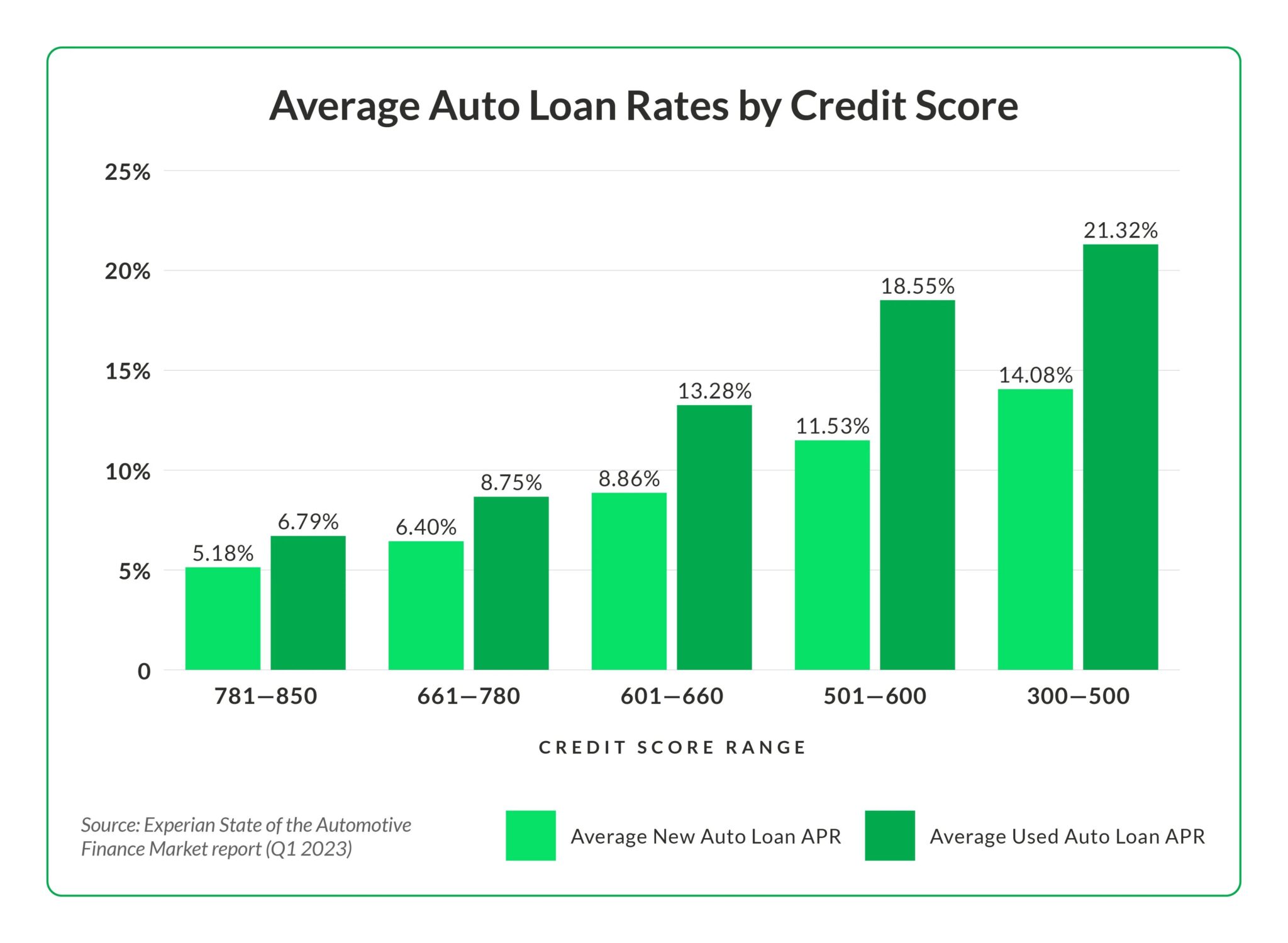

In fact, your credit score can help you determine if now is a god tiod time to buy a used car, or possibly even the worst time. Used car loan rates now average north of 13% APR. But that’s just the average. Shoppers with lower credit scores (under 650) will only qualify for higher rates, perhaps approaching 20% APR for the lowest scores, if you can get qualified at all.

Check out the 2023 data from Experian via MarketWatch to see the average auto loan rates by credit score. This is very similar to what shoppers should expect today, as rates have remained high over the past year.

How much does interest rate matter with a used car loan? Let’s look at a realistic example. With a $30,000 car loan over 72 months, the difference in interest paid between a loan at 5% APR and one at 15% APR is substantial. It’s always best to opt for a shorter loan term, but we’ll use this example since more drivers are stretching out their payments as prices rise.

What’s the difference in interest paid? With a 5% APR, you would pay approximately $4,776 in interest over the 72 months of the loan. However, at a 15% APR, the interest spikes to $13,632, resulting in an additional $8,856 in interestcosts. This highlights the significant financial impact that APR can have on the total cost of a loan.

No matter when you get serious about buying, DO NOT overlook the power of having a good credit score. It’s the difference between paying a little interest, and eye-gouging amounts owed month after month.

For more about what credit score car dealers and banks use, check this out.

2. Know Your Budget

The reality of 2024 is stark: cars are more expensive, and finding a reliable, low-mileage vehicle under $10,000 is virtually impossible. According to research from iSeeCars, while 49.3% of all used cars were priced under $20,000 in 2019, today that number stands at just 12.4%.

Before you fall in love with a make or model, use tools like CarEdge’s Car Search to set realistic expectations and shop within your means.

If you’re not in urgent need of transportation, waiting might be wise. We anticipate used car prices could drop an additional 2-5% later in the summer and potentially even more towards the end of the year. Delaying your purchase could save you thousands, especially if interest rates begin to decrease as predicted. Although with inflation staying stubbornly high, the general consensus is that interest rates will remain at current levels for at least a few more months, if not longer.

So Is Now a Good Time to Buy a Car? CarEdge’s Advice for 2024

Deciding whether to buy a used car now or later in 2024 boils down to your personal circumstances—your budget, your credit score, and how urgently you need a vehicle. If your situation allows, waiting a few months could be financially beneficial, both in terms of lower prices and potentially reduced interest rates. This is especially true if you could use more time to improve your credit score. Qualifying for the best rate possible will save you thousands in interest payments with most used car loans today.

However, if you need a car soon, finding a well-priced deal now is possible IF you’re prepared to negotiate. Check out the free tools below! And remember to use CarEdge Insights to equip yourself with local car market data. You’ll negotiate like a pro in no time!

So overall, is now a good time to buy a used car? The answer is that it’s an okay time, and better times are ahead once prices drop further, and these insanely high interest rates come down. But the future is notoriously hard to predict. If you need a ride quickly, you CAN score a deal with negotiation know-how.

Free Car Buying Help Is Here

Navigating the used car market can be complex, but with CarEdge, you’re never alone. Ready to outsmart the dealerships? Download your 100% freecar buying cheat sheets today. From negotiating a deal to leasing a car the smart way, it’s all available for instant download. Get your cheat sheets today!

Stay tuned to CarEdge for more insights and tips on car buying in 2024!

Shopping for a new car is an exciting time, but knowing which brands to steer clear of can save you from a lot of future headaches. At CarEdge, we’re diving deep into rankings from Consumer Reports, and complimenting their legendary work with our own car market updates from CarEdge Insights. Here’s a breakdown of the 10 least reliable car brands in 2025. If you buy one of these cars, you ought to have a car maintenance emergency fund at your disposal, or start getting quotes for extended warranty protection!

Consumer Reports’ 2025 Reliability Rankings: The Least Dependable Car Brands

We hope you enjoy the real-time car market data we’ve included. Head over to CarEdge Insights for localized data that YOU can use to negotiate effectively.

Consumer Reports provides an annual snapshot of car reliability, all based on data from over 300,000 vehicles that addresses 17 common trouble areas. The non-profit has been helping car buyers make smart choices for 88 years. In 2025, the CR rankings reveal a few brands that, well, might not be your best bet if reliability tops your priority list. For comparison’s sake, we’ve also included the number of recalls for each manufacturer over the past year ending in January 2025, via the NHTSA.

Although Rivian is the least reliable car brand according to Consumer Reports, all GM brand rank near the bottom. Here’s a look at the car brands most likely to give you problems during ownership.

The Least Dependable Car Brands Surprisingly Don’t Have Much In Common

From frequent breakdowns to excessive recalls, these brands show various signs of potential trouble for consumers. Surprisingly, the least reliable car brands are often expensive. With the likes of Rivian, Tesla, Volvo and Volkswagen on the list, it’s clear that when it comes to reliability, you don’t always get what you pay for.

Other than that, we see a mix of manufacturers from around the world on this unfortunate list. In a massive improvement from last year, only one Stellantis brand is on the list. General Motors, on the other hand, had falling reliability ratings, with three of the four GM brands on the bottom 10. Chrysler, the only GM brand not making an appearance, wasn’t rated by Consumer Reports due to ‘insufficient data’.

According to Consumer Reports, hybrid vehicles lead the pack among electrified powertrains in terms of reliability. “On average, hybrid powertrains remain reliable, while pure electric vehicles (EVs) and plug-in hybrid vehicles (PHEVs) are improving despite continuing reliability problems.”

On the other hand, plug-in hybrid vehicles tell a different story, facing 70% more issues than gasoline (ICE) vehicles. Consumer Reports found that fully electric vehicles (BEVs) have 42% more problems than gas-powered or traditional hybrid vehicles. This is a big improvement from last year, when EVs had 79% more issues than ICE vehicles.

Want Free Car Buying Help in 2025?

While it’s crucial to consider reliability, don’t forget to weigh other factors such as fuel efficiency, safety features, and overall cost of ownership. Check out our detailed CarEdge cost of ownership rankings to get a fuller picture.

Ready to outsmart the dealerships? Download your 100% freecar buying cheat sheets today. From negotiating a deal to leasing a car the smart way, it’s all available for instant download. Get your cheat sheets today!

As we enter the heart of spring, car shoppers have every reason to mark their calendars for Memorial Day weekend (May 25 – May 27). Traditionally a hotbed for great car deals, 2024’s Memorial Day sales are poised to be especially big. This year, high new car inventory levels and expensive floorplanning costs for dealers are setting the stage for big bargains.

Inventory Is Still High, and That’s Good News For Buyers

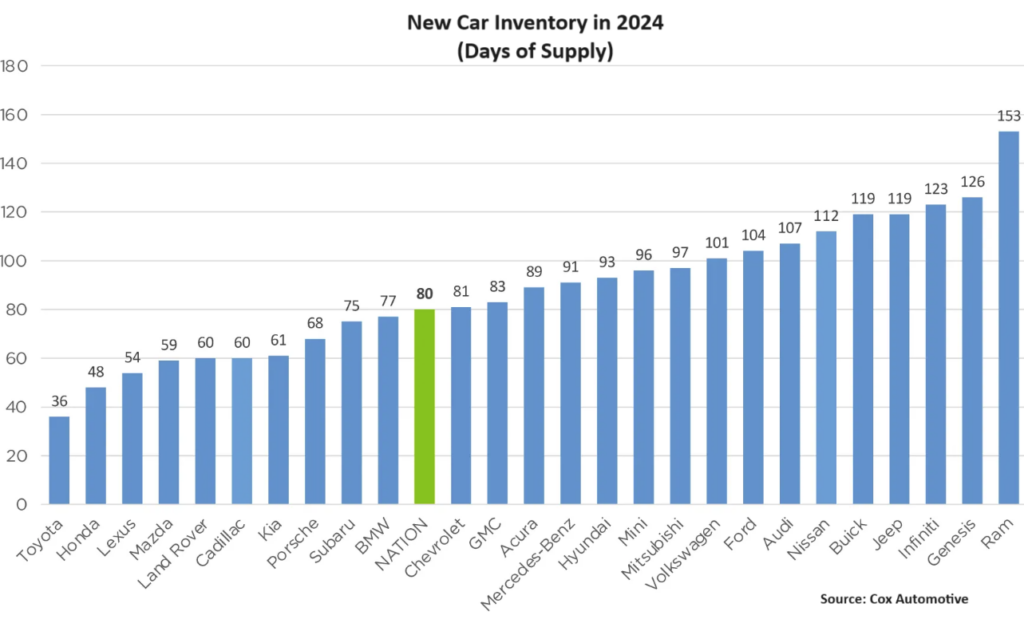

Most automakers are grappling with unusually high levels of new car inventory. According to Cox Automotive, April opened with 72 days of new-vehicle supply industry-wide, a notable increase of 46% compared to a year ago. This glut stems largely from a mismatch between production outputs and a softening consumer demand, influenced by lingering economic uncertainties, high interest rates, and in many cases, ridiculously high MSRPs.

This overstock is particularly pronounced in the truck, SUV, and luxury vehicle sectors. While sales in 2024 are indeed picking up—showing an 11% increase in March compared to the previous year—the rising sales figures are not enough to offset high inventory levels. But that’s what OEMs hope to change with May’s best car deals.

Last Year’s Models Are This Year’s Deals

Manufacturers are under pressure to clear out 2023 models, four months into the new year. In late April, 300,000 of the nearly 3.1 million new cars for sale in America were 2022 or 2023 models. Many of them are trucks like the Ford F-150 and Ram 1500. Even with thousands of 2023s on dealer lots, manufacturers are flooding dealer lots with more inventory (more on that here).

This pressure is not just a warehouse issue; it’s a financial imperative. High floorplanning costs driven by stubbornly high interest rates are eating into dealer profits, adding to the sense of urgency.

Car Brands On Track For Big Memorial Day Sales

Despite the modest gains in sales, certain brands like Ram, Jeep, Mazda, Ford, and Nissan are facing significant inventory excesses compared to their competitors. These brands are likely to offer bigger discounts for Memorial Day as they strive to sell cars.

Car brands with less inventory include Toyota, Subaru, and Honda. These brands are less likely to offer big incentives in May.

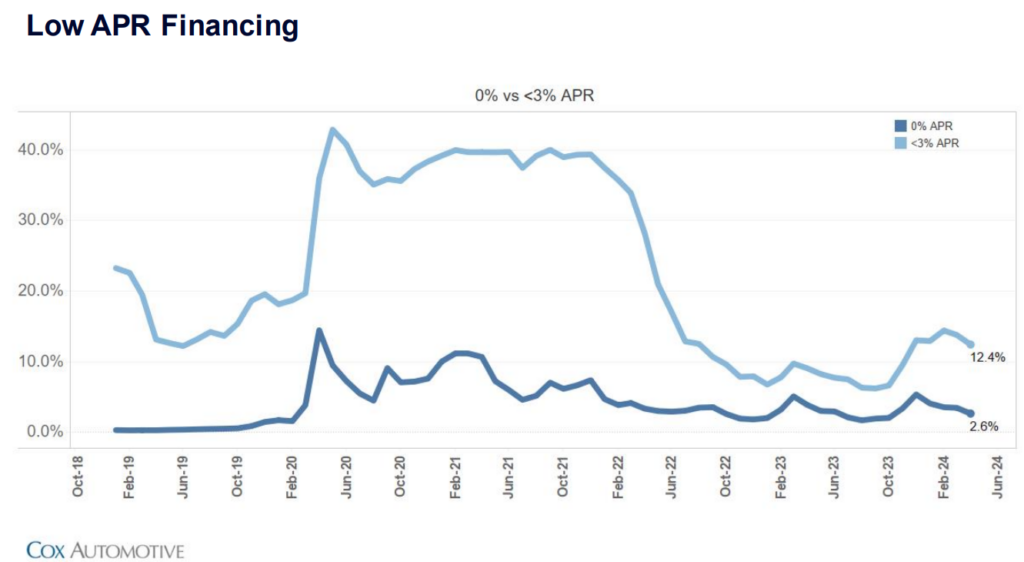

Low APR deals are a win-win for both dealers and buyers. For dealers, it’s about liquidating stock without slashing sticker prices dramatically, which can devalue the brand. For buyers, these subsidized rates lower the monthly payment, making an upgrade more feasible. Expect to see APR offers as low as 0% for qualified buyers on select models, alongside generous cash-back offers and lease deals.

In fact, there are already several 0% APR offers on the market today…

As we inch closer to Memorial Day, certain vehicles stand out for their negotiability. While the specific models and deals will be confirmed as the holiday approaches, here are some categories to watch:

Last Year’s Inventory: Memorial Day car sales are the manufacturer’s best chance to clear out the last of 2023’s remaining inventory. Expect crazy deals on these, especially trucks and the most negotiable electric vehicles.

Truck Deals: Automakers have simply priced new trucks too high, and buyers are pushing back. This has led to an oversupply of new trucks on dealer lots. Expect big deals on the Chevrolet Silverado 1500, Ram 1500, and Ford F-150. In fact, there are already some great low APR offers out there. Check out the truck deals here.

Electric Vehicles: Despite their steadily growing popularity, certain EV models are still struggling to find their market footing, leading to potentially larger discounts. The Ford Mustang Mach-E and F-150 Lightning, Nissan Ariya, and electric offerings from Hyundai and Kia are all slated for big discounts and low APR offers in May.

Gear Up for the Deals

This Memorial Day, CarEdge is your go-to resource for navigating these sales. Not only will we provide a one-stop resource for the best car sales, we’ll also share car market insights that you won’t find anywhere else. 👉 Bookmark this page and check back in early May to see what automakers have to offer!Head to this page for the best deals right now, no matter when you’re reading this.

For many, there will eventually come a time when you need to part ways with a beloved car – even when you still owe money on it. Selling a car with an outstanding loan can seem daunting due to the added complexity of dealing with lenders. However, with a proper understanding of the process and careful planning, you can navigate the situation with ease. Here at CarEdge, we’re diving into how you can efficiently and effectively sell your car, even if the loan isn’t fully paid off yet.

Step One: Understanding Your Loan Details

When you’re considering selling a car that you still owe money on, the first crucial step is to fully understand the details of your loan. This knowledge is not only essential for setting the right sale price but also for ensuring that the transaction is handled legally and smoothly.

First thing’s first: understand your loan. That means digging up your login credentials to get into your online account with the lender. You may even need to give them a call, or hop on the live chat.

Here’s what to figure out before selling your car with a loan balance:

Check Your Loan Balance: Log in to your account, or contact your lender to request the current balance and the official payoff amount of your loan. The payoff amount may be higher than the balance due to the inclusion of any prepayment penalties or accrued interest.

Understand the Payoff Process: Ask your lender about the specific steps required to pay off the loan. You need to know how long it takes for them to process payments and release the lien. This timing is critical, especially if you need to coordinate with a buyer.

Lienholder Details: While your lender holds a lien on your vehicle, making them a key stakeholder, you don’t need their explicit permission to sell the car. However, you do need to pay off the loan. When you send the payoff check to your lender, include a signed payoff authorization form. This form authorizes the bank to send the lien release or the physical title directly to the new owner. By doing this, the buyer is protected, knowing that the necessary documents to prove ownership will be sent to them by the bank.

Obtain a 10-Day Payoff Quote: Most lenders will provide a quote that is valid for 10 days, which includes the total amount required to pay off your loan in full as of that date, including any additional fees or accumulated interest. This quote will be vital when you finalize the sale and need to settle the loan balance.

Step Two: Valuing Your Car

Next, determine how much your car is worth. Use trusted resources like Edmunds or Kelly Blue Book, and use CarEdge’s valuation tool to see how much online buyers will pay.

If you decide to go the private seller route, it’s important to price your car thoughtfully. Remember, you’re trying to sell the car quickly while also covering your remaining loan balance. Setting the right price can help you attract buyers quickly while ensuring you don’t fall short financially.

Step Three: Finding a Buyer

You have two main avenues for selling your car: a private sale or a dealership trade-in. A private sale typically yields a higher return but requires more effort on your part in terms of marketing and negotiation. Platforms like Facebook Marketplace, Cars.com, and AutoTrader are great for reaching potential buyers. On the other hand, trading in your car at a dealership is less hassle but is highly unlikely to offer as much for your car, especially with an outstanding loan.

With a dealership trade-in, it’s common to be offered 20-30% less than your car is worth in a private sale. If you could really use that additional money, going through the longer, more tedious process of selling privately may be worth it.

The financial aspect of selling a car with an outstanding loan can be tricky. But don’t give up now! If you’re eager to sell, it’s worth the hassle. Here’s how to handle it effectively:

Escrow Services: Using an escrow service for a private sale is strongly recommended as it adds a layer of security for both parties. The escrow service will hold the buyer’s payment until the loan is paid off and the lien is released, ensuring that the buyer doesn’t hand over money without securing the title, and you don’t transfer the title without clearing the loan.

Addressing Shortfalls: All payoff should be made with a cashiers check to further expedite the process. If the selling price doesn’t cover the loan payoff amount, you will need to provide the additional funds to clear the loan. Consider your options for covering this shortfall, such as a personal loan or a line of credit.

Payment to Lender: If you go this route, be sure to confirm that the buyer is comfortable with it before sealing the deal. It’s possible to coordinate with the buyer on making the payment directly to the lender. However, with a properly filled out payoff authorization stipulating that the documents go to the buyer, this would not be necessary.

Handling Overpayments: If the car sells for more than the payoff quote, plan how the surplus will be handled. Confirm with your escrow service (or with the buyer if they will pay your lender directly) to return the excess amount to you after the loan settlement.

Documentation: Keep meticulous records of all communications and transactions related to the loan payoff and car sale. Documentation should include the final payoff receipt from your lender and any agreements made with the buyer.

Step Five: Transfer of Ownership

Transferring ownership involves a few small hurdles, but it’s nothing you can’t do! You must inform the buyer about the lien and ensure that the loan is fully paid before transferring the title. Even with a lien, you are legally required to provide the buyer with a bill of sale, documenting the transfer of ownership to the buyer. Alongside this, include a payoff authorization when you send the loan payoff to your lender. This authorizes them to release the lien or send the physical title directly to the new owner. Once you receive a lien release from your lender, you can complete the title transfer to the new owner.

Each state has different laws, so it’s important to check your local requirements. Check with your state DMV. The information should be easily found on their website.

If you want to avoid these hurdles, consider paying off the loan balance and securing the lien release before you sell the car. This approach eliminates many potential complications that could delay the sale.

Plan Ahead to Avoid Headaches (You’ve Got This!)

Selling a car with an outstanding loan requires careful attention to financial details and diligent record-keeping. With the right approach, you can sell your loan and transfer ownership without a hitch. Remember, knowledge is power in any transaction. Understanding how to handle this process can save you from potential financial pitfalls. For more insights and resources on managing car sales and ownership, keep it tuned to CarEdge.

👉 Want to become a car market pro? How about that and more for FREE?

Sign up for Deal School today, our free course for anyone interested in buying, selling, or simply owning a car the smart way.

It seems like there’s finally some good news on the horizon for potential car buyers. The latest car market data indicates a promising downward trend in new car prices. Let’s dig into what’s happening and why it might be the perfect time to consider that new car purchase.

Relief… To An Extent

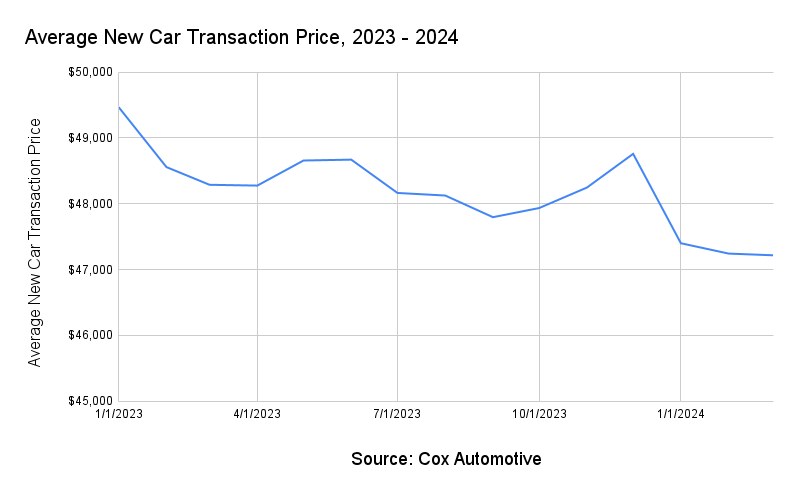

New data from Cox Automotive confirms that new car prices are dropping this spring, a trend that’s likely to continue into summer. For the first time in nearly two years, new-vehicle average transaction prices have dipped to their lowest, standing at $47,218 in March. This is down 1% from last March and a substantial 5.4% from the market peak in December 2022. It seems like the relentless price surge is taking a breather, giving buyers a much-needed respite.

Contributing Factors

Several factors are driving falling car prices. A significant recovery in new-vehicle supply has bolstered sales results. Inventory levels at the start of March were about 2.7 million units, showing a 52% increase year over year. More cars on lots mean more competitive pricing and better deals for consumers.

Incentives are also playing a big role. The average incentive spend from manufacturers increased 11% to $3,121, reaching the highest level since May 2021. With incentives accounting for 6.6% of the average selling price, it’s clear manufacturers are keen to move cars off lots.

Interestingly, even with slightly lower prices, affordability remains a hurdle due to historically high interest rates. The typical new vehicle loan interest rate now sits at 10.47%. Surprisingly, the average monthly payment is down by 1.2% to $744. That’s still up 40% from 2019, when the average monthly car payment was $533.

When you combine car loan interest rates with the modern era’s high MSRPs, the result is massive interest payments. At today’s average APR of 10.47% and an average selling price of $47,218, a 72-month loan would result in about $15,000 in interest over the 6-year loan term.

How can car buyers avoid interest charges? Here are a few foolproof ways to lower your interest payments.

Larger down payments

Take advantage of APR offers

Keep your credit score in top shape

Avoid longer loan terms – stick to 60 months or less

Buying used? Compare rates from trustworthy credit unions

Too Many Luxury Cars, Too Few Budget Models

Automakers always aim to make more money, even if that means alienating some of their customer base. In recent years, this has meant abandoning low-margin affordable models, and replacing them with luxury cars and trucks that are more profitable.

For example, Nissan is discontinuing the Altima next year, yet continues to push $60,000 EVs that are selling poorly.

The shift towards luxury vehicles and higher-priced models complicates car buying for the average consumer. According to Cox Automotive, out of approximately 275 new-vehicle models available in the U.S., only eight had average transaction prices below $25,000, and only two were under $20,000—namely, the discontinued Kia Rio and Mitsubishi Mirage. Contrast this with March 2021, when over 20 vehicles routinely transacted below $25,000.

Additionally, the number of vehicles transacting at prices over $100,000 has increased significantly, with 30 different models in this bracket last month alone.

Is It a Good Time to Buy a Car?

With prices down, incentives up, and a decent dip in monthly payments, this could be a strategic time to consider a purchase, especially if you’ve been on the fence. Our team of experts is confident that this summer will be a better time to buy, if you’re patient. And if you can wait even longer, year-end deals are always the best.

With interest rates still high, insurance premiums climbing, and selling prices averaging over $47,000, it’s crucial to calculate your finances carefully. Remember, it’s a lot more difficult to find a new car for under $25,000 than in years past. Budget for ALL expenses that come with a new or used vehicle, from payments to fuel, maintenance, and insurance.

States eligibile for below invoice pricing and 100% free delivery:

Alabama, Arkansas, Texas, Oklahoma, Florida, Georgia, Kentucky, Louisiana, Maryland, Delaware, Mississippi, North Carolina, South Carolina, Tennessee, Virginia, and West Virginia.

What if I don’t live in these states? If you're outside these areas, don't worry! We're committed to making sure everyone can enjoy our deals. Although the delivery fee will not be waived, you can still purchase from CarEdge and either pay for shipping or coordinate pickup at a participating dealer.

Getting Started!

Please enter the following information to generate a price-transparent price quote.

FAQ

How much does it cost?

Our concierge service costs $999 plus an optional shipping fee (based on distance or pick-up).

To get started, pay the one-time payment of $999 and a CarEdge concierge will start by negotiating the vehicles in your favorites.

Why should you let a concierge do the work?

Get the best deal

Our team of concierges and industry experts with 75+ years of combined experience with access to tools and data to leverage the best deal possible.

Convenience

Gone are the days of looking for a car and stepping into the dealership spending hours and hours of head banging only to get smooth talked into a higher price.

Expert assistance

We answer all questions you may have regarding the buying process, what the right car is, the deal itself, and more!

Who are the concierges?

Transparent when others aren't

Our commitment to transparency and honesty ensures that you make informed decisions, while our years of experience guarantee that we will be able to secure the best deal for you.

When you win, we win

We work for you, not the dealership, ensuring your interests are always our top priority.

Buying a car just got a whole lot easier.

What happens next?

We’ll coach you on how to get dealers competing to get the best price

You’ll get instant access to our car buying checklists, guides, and market insights

What’s included in my car buying toolkit?

Dealer Invoice Price

Access the Dealer’s Invoice Price to negotiate an even better car deal.

Target Discount

A recommendation of for how much you should negotiate towards.

Negotiation Guide

Know exactly what you need to say to dealers to secure the best deal.

Exclusive Data

Info about your car such as cost of ownership, sales data, and more!