Get access to the same vehicle valuation tool that dealers rely on. With Black Book, you’ll have insider data to accurately assess trade-in and purchase values—empowering you to negotiate the best possible deal.

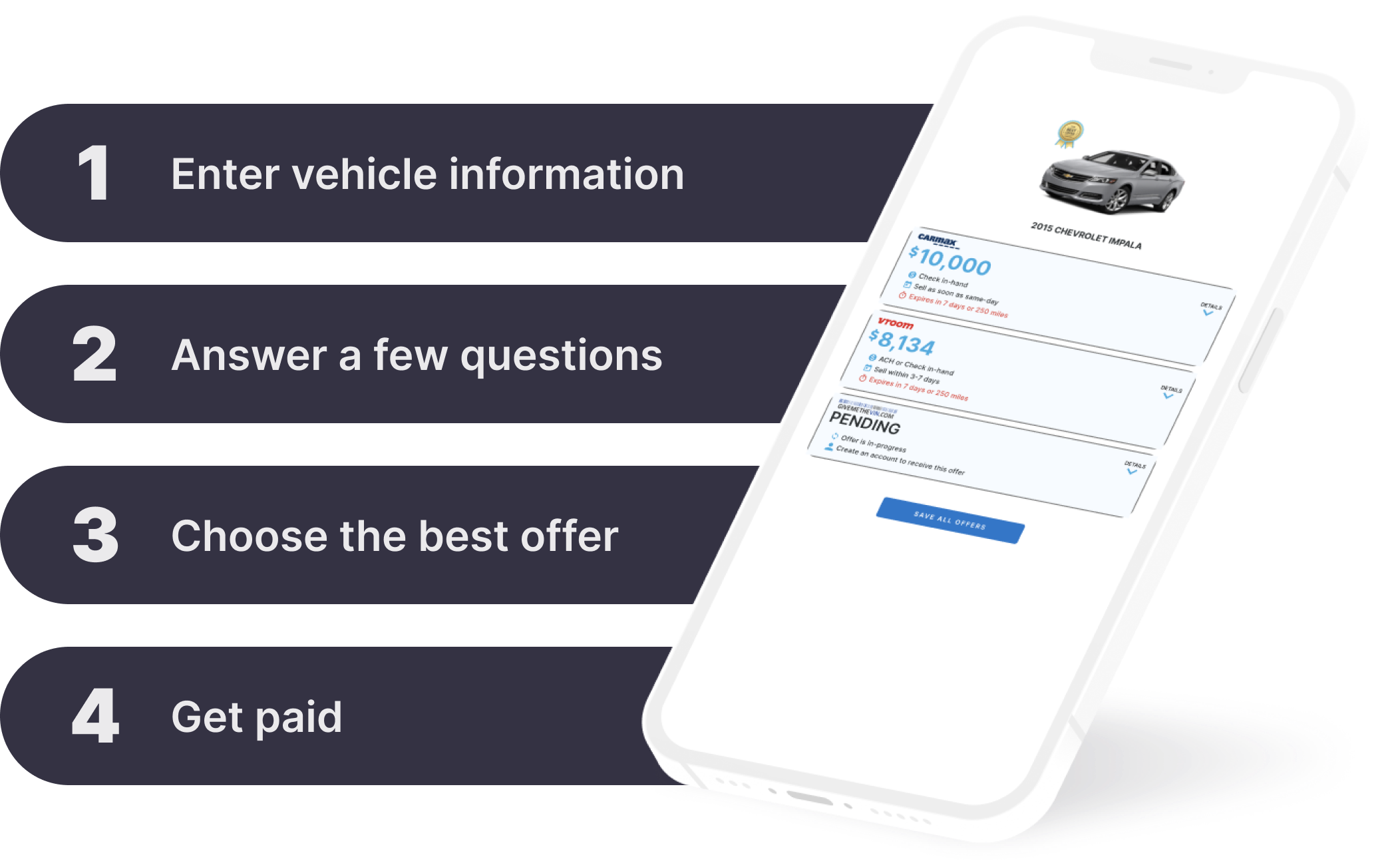

If you’re looking to sell your car quickly and hassle-free, getting an instant cash offer for a car can be one of the easiest ways to do it. Instead of haggling with private buyers or trading in for a low-ball offer, these online platforms provide an upfront price based on your vehicle’s details. But which services are worth considering? We’ve reviewed five of the best options to help you get the most for your car in 2025.

CarEdge – Compare Offers and Skip the Dealership

Summary:CarEdge provides a transparent process for selling your car by offering market-based pricing insights and connecting you with vetted buyers. With a data-driven approach, CarEdge ensures you get a competitive instant cash offer while giving you the tools to make an informed decision.

CarEdge’s instant cash offer is sourced from three trusted partners: Peddle, givemethevin.com, and webuyanycar.com.

Pros:

Easiest way to compare cash offers from multiple online car buyers.

Black Book vehicle values are available through CarEdge, helping you know if you’re getting a fair instant cash offer.

Cons:

New in the game, but growing quickly.

Offers from others, like CarMax and Carvana, will have to be requested separately.

The Verdict: CarEdge is a great choice for sellers who want a transparent, data-driven approach to getting the best instant cash offer for their car.

CarMax – A More Traditional Experience

Summary:CarMax is a well-known brand that offers a straightforward process for selling your vehicle. By entering your car’s details online, you’ll receive an instant cash offer that you can redeem at any of the 253 CarMax locations nationwide. The offer is valid for seven days, giving you time to compare deals.

Pros:

Convenient nationwide locations make it easy to complete the sale in person.

No obligation to sell, so you can shop around for a better offer.

Your offer is good for seven days.

Cons:

In-person visit required to finalize the deal.

For some, selling to CarMax can end up feeling like the dreaded dealership experience.

Lower offers are common, as CarMax resells cars at a profit.

The Verdict: CarMax is a great option for those who prefer an established company and don’t mind visiting a physical location to complete the sale. However, it can come with the unpleasant dealership experience that most drivers prefer to avoid.

Carvana – A Well-Known Name with Fluctuating Offers

Summary:Carvana provides a completely online selling experience. You enter your car’s details, receive an offer, and if you accept, Carvana will pick up your vehicle and issue payment, with no need to visit a dealership. Note that Carvana’s instant cash offers are known to fluctuate from day to day.

Pros:

Fully online process, making it convenient and hassle-free.

Fast payment, with most sellers getting paid right after pickup.

Cons:

Limited physical locations, so support is primarily online.

Offers fluctuatewidely based on market demand and inventory needs.

The Verdict: Carvana is a good option for sellers who want a fully digital, contact-free process. However, sellers should be aware that offers can fluctuate wildly day to day, depending on market conditions. Compare quotes from other instant cash buyers before you commit.

Kelley Blue Book – Dealership Visit Required

Summary:Kelley Blue Book (KBB) provides a tool that generates an instant cash offer based on your car’s details and market value. This offer can be redeemed at participating dealerships after an inspection.

Pros:

KBB is a widely respected name in the automotive industry.

Multiple participating dealerships, allowing you to compare offers.

Cons:

You still have to go to the dealership.

Offer may change after an in-person inspection.

Not all dealerships participate, which limits availability in some areas.

The Verdict: KBB Instant Cash Offer is a great option for those who prefer to sell their car through a well-known website with multiple dealership options. It’s not recommended for sellers who prefer to stay away from the dealership experience.

EchoPark – $250 Bonus, But Limited Locations

Summary:EchoPark provides an instant cash offer online, valid for seven days or 500 miles. If you sell your car to EchoPark within 48 hours of receiving the offer, they’ll add an extra $250 to your payment. However, you must bring your car to an EchoPark location to finalize the deal.

Pros:

Bonus incentive of $250 if you sell within 48 hours.

No obligation to buy, meaning you can sell your car outright without trading it in.

Cons:

Limited locations, so availability varies by region.

In-person visit required to complete the transaction.

The Verdict: EchoPark is a strong option for sellers who live near one of its locations and want to maximize their offer with the $250 bonus incentive.

Which Instant Cash Offer is Best in 2025?

The best option depends on your priorities. If you want the best offer without dealership hassles, CarEdge is a great option. With CarEdge’s car value tracking tool, you can see your car’s value change in real time. This makes it easier to decide when to sell. If you prefer a traditional dealership experience, CarMax or KBB Instant Cash Offer could work better. For those near an EchoPark location, the extra $250 incentive makes it a great pick.

Ultimately, all sellers should compare offers from each of these online car buyers to see where the best deal is. Instant cash offers for cars can vary widely from one buyer to the next.

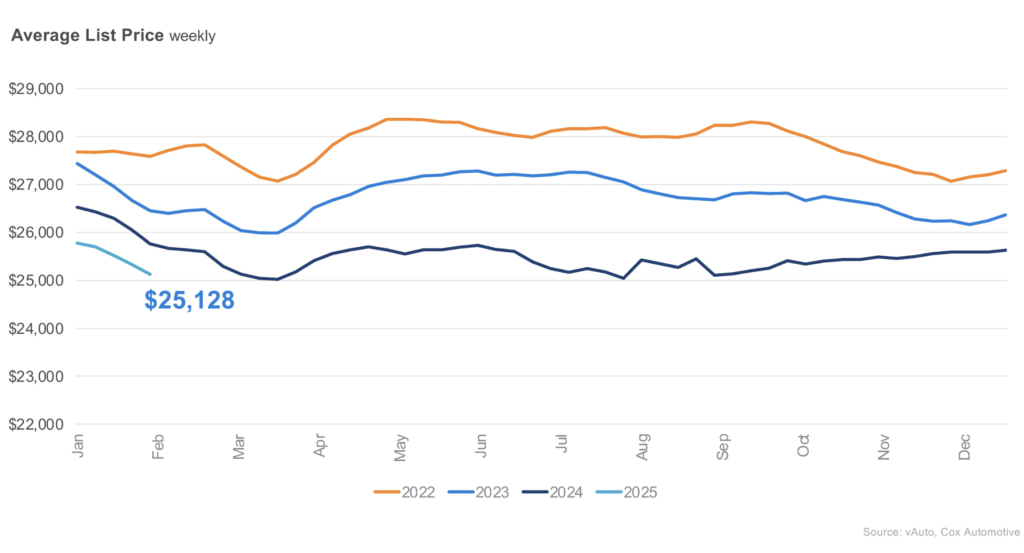

Spring is just around the corner, and if you’re in the market for a used car, you might want to think strategically about when to buy. The worst time to purchase a used car is fast approaching, as prices historically rise in late March, April, and early May when demand surges. On the flip side, if you’re thinking about selling, spring is the perfect time to get the most for your car.

Here’s everything you need to know about where the used car market stands heading into spring 2025.

Used Car Prices Will Rise Soon – Here’s Why

While used car prices have come down from their record highs in 2022, they’re still well above historical norms. As of February 2025, the average used car selling price is $25,128. That’s $5,000 higher than just five years ago. However, our weekly used car price updates show that selling prices have been slowly falling in early 2025. As we head into spring, seasonal trends are on track to send prices the other direction. With spring car-buying season ahead, prices are about to climb higher,

Several factors are expected to drive used car prices higher for spring 2025:

Tax Refund Season Fuels Demand – Many buyers use tax refunds for down payments, creating a rush of demand in March, April, and May.

Lower Inventory at Affordable Price Points – Used cars under $15,000 are in short supply, with only a 35-day supply on the market. That’s nine days lower than last year, according to Cox Automotive.

New Car Prices Keep Climbing – As automakers continue to push new car prices higher, more drivers are shopping used car lots in search of affordability. As preowned lots get crowded with shoppers, negotiations become more challenging.

Top Brands Are the Most Competitive – Used Ford, Chevrolet, Toyota, Honda, and Nissan models made up 51% of all used cars sold last month. Because these brands are in high demand, prices are expected to rise the most in the spring.

A look at the best-selling used cars

Here’s a look at the average selling prices of the top 10 used cars in America in 2025, courtesy of CarEdge Insights:

Make

Model

Average Selling Price (Used)

Days of Supply (Used)

Ford

F-150

$29,591

61

Chevrolet

Silverado 1500

$29,212

60

Toyota

RAV4

$23,794

52

Tesla

Model Y

$30,999

37

Honda

CR-V

$20,010

50

Ram

1500

$29,500

64

GMC

Sierra 1500

$33,500

60

Toyota

Camry

$20,589

58

Nissan

Rogue

$19,498

59

Honda

Civic

$16,495

55

Although used car and truck prices have fallen from recent highs, they still remain far above historical norms. Car prices have exceeded the rate of inflation over the past 5 years, adding insult to injury for household finances.

Today’s used car buyers are unsurprisingly finding the best deals on higher mileage vehicles. As drivers hold on to vehicles longer, the odometer readings continue to creep higher. The average used car on sale in the U.S. has 70,000 miles on the odometer, a new all-time high. It’s more important than ever to get an independent Pre-Purchase Inspection on ANY used car before buying.

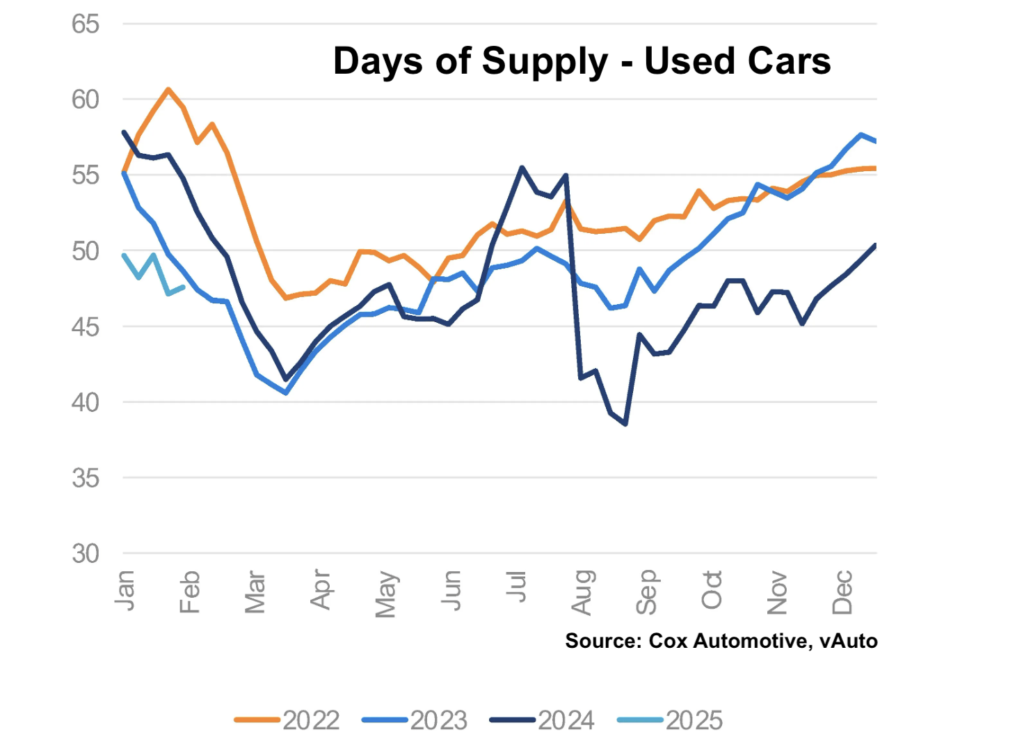

Used Car Inventory Is Tight – And It’s Getting Tighter

Another reason prices will keep rising? There simply aren’t enough used cars on the market.

Total used car inventory is down 3% year-over-year. There are currently 2.23 million used cars for sale in the U.S., compared to 2.5 million three years ago. The lingering effects of pandemic-era production shutdowns continue to impact supply, with fewer used cars available today.

Days of supply shows a tightening market. Right now, the market has a 48-day supply of used cars, down from 56 days at this time last year. With demand about to spike, this will shrink further, making it harder to find the right car at a great price.

If you’re shopping for a used car, expect inventory to tighten and prices to rise as we enter spring. Basic supply and demand principles lend themselves to higher used car prices in late March through early May.

Used Car Loan Rates Remain High

Financing a used car in 2025 comes with a major challenge: high interest rates. The average used car loan rate is still hovering around 14% APR, making it tougher for buyers to afford monthly payments. Even those with excellent credit are struggling to find rates below 7% APR, even when financing through credit unions and local banks.

Unfortunately, relief isn’t on the horizon. The Federal Reserve has signaled that future interest rate cuts are on hold due to persistent inflation. That means used car loan rates are likely to remain elevated for the next several months.

💡 CarEdge Tip: If you need to finance a used car, shop around for the best rates before stepping foot in a dealership. Comparing offers from multiple lenders—especially local credit unions—can help you secure the lowest possible rate.

Spring Is the Best Time to Sell a Car

While buyers face a more competitive market, spring 2025 is an excellent time to sell a used car or trade one in.

More buyers = better offers – With demand increasing, used car sellers will have more negotiating power, whether selling to a private buyer or trading in at a dealership. Sellers who are familiar with seasonal trends in used car prices are more likely to get a fair offer.

Higher trade-in values – As dealers have a harder time sourcing inventory, trade-in offers will be more competitive, especially for popular brands like Toyota, Honda, Subaru, and Ford.

Bottom Line: Should You Buy a Used Car in March 2025?

✅ If you need a car soon – Act fast before prices climb higher. If you’re set on buying this spring, compare listings now and lock in a deal before demand spikes.

⏳ If you can wait 90 days – Consider holding off until late May or early summer, when the spring surge settles and inventory stabilizes.

🚗 If you’re selling – Spring is the time! Take advantage of high demand and strong trade-in values before the market shifts come summer.

Being upside-down on a car loan, also known as having negative equity, is a stressful situation. It means you owe more on your car loan than your car’s current market value. This can happen due to factors like rapid depreciation, unfavorable loan terms, or rolling over previous negative equity into your current loan.

For example, if your car is worth $15,000 but you still owe $20,000, you’re upside-down by $5,000. As distressing as negative equity loans can be, it’s not uncommon. CarEdge’s recent Negative Equity Report found that more than one-third of drivers who financed have underwater auto loans.

The good news is that there are several strategies you can use to part ways with your underwater loan as quickly as possible. We’ll explore practical ways to get rid of a car with negative equity, helping you make an informed decision each step of the way.

How to Get Rid of a Car With Negative Equity

Looking to sell your car with negative equity as soon as possible? Here are a few proven strategies to consider, depending on your financial situation and goals.

1. Sell Your Car

If you’re serious about getting rid of your car, it is possible to sell a car with negative equity. If you’re looking to sell your car without trading it in at a car dealership, you’ll need to pay the difference between the sale price and your loan balance to settle your current loan when you sell your car. Check out our Complete Guide to Selling a Car with a Loan.

You’ve got a few options for selling your car, even if you have negative equity.

Private Sale

Selling privately often yields a higher price than trading in at a dealership. However, you’ll need to pay off your existing loan before selling. Most of us don’t have that much cash on hand, but luckily there’s still a way to make it work. If you have great credit and proven income, you may be able to obtain a personal loan to pay off the loan balance. After the car is sold, you can use the proceeds from the sale to immediately pay off your personal loan.

Private sales offer an advantage for older cars or vehicles with higher mileage because you can often command a higher selling price with a private buyer than what a dealership would offer. Remember that dealerships are likely to wholesale these types of vehicles, as they may not be able to retail them on their lot due to higher reconditioning costs and lack of financing options for these vehicles.

Newer late-model, low mile vehicles are difficult to sell to private party buyers because they don’t usually have the cash on hand to make large ticket purchases and will need to rely on financing options that are more readily available at licensed dealerships.

👉 Pro Tip: To determine the selling price for a used vehicle in a private party sale, have an appraisal done in person at Carmax and then add $2,000 to $2,500 to the written offer.

Sell to an Online Buyer

You can sell to online car buyers like Carvana, CarMax, and AutoNation, and Driveway without being required to purchase a vehicle from their store. These large Auto Groups will quickly appraise your vehicle (online or in person) and provide a conditional cash offer. While this option is highly convenient, understand that you’re unlikely to get as much for your car as you would with a private sale. If you’re deeply underwater, online buyers may either require you to pay the difference between the loan balance and sale price, or they may refuse to buy your car. However, this is a solid option for many.

Late-model, low-mileage cars in top condition are attractive to dealerships because they will retail them on their lot and be able to offer financing and other warranty products to maximize their return. However, to secure a fair market value, you need to shop around for the best offer.

When shopping for a replacement vehicle at a licensed dealership, you may have the option to roll any negative equity into the balance of the new loan, provided that the loan-to-value ratio meets the lender’s requirements. ⚠️ Beware,car buyers who roll over negative equity into a new loan are likely to end up in a similar situation in the future.

👉 Pro Tip: It’s fine to mention that you might have a trade-in during the negotiation of your replacement vehicle’s selling price. However, to maximize your trade allowance, avoid sharing detailed information with the dealership until you have 1) obtained an appraisal from a reputable brick-and-mortar store like Carmax, and 2) have first finalized the selling price of the replacement vehicle.

Pros of Selling Your Car:

Frees you from the car and loan and eliminates your financial responsibility.

Private sales can get you more than expected for your car, but it’s usually best to pay off the loan first.

Cons of Selling Your Car:

Selling a car with negative equity requires cash to cover the gap between the sale price and the loan payoff balance.

Trade-ins may lead to higher debt on a new car, and often lead to another underwater loan.

If you can’t afford to pay off the gap between your loan balance and the car’s resale value, but you’re determined to sell, rolling over your loan is an option if you’ll be needing another vehicle. Rolling over negative equity involves trading in your car and adding the remaining loan balance to your next loan. While this solves the immediate issue, it often leads to a cycle of debt. It can be a viable option if your next vehicle is much more affordable (and with more affordable payments) than the car you’re coming out of.

Pros:

Immediate solution to get rid of the car.

May provide access to a more reliable and more affordable vehicle.

Cons:

Increases the loan balance on your next car.

Leads to higher monthly payments and longer debt obligations.

It is very easy to end up in years of additional negative equity when rolling over loans.

3. Not Recommended: Voluntary Repossession

If you’re deeply underwater on your auto loan, must get rid of your car, but can’t afford to pay the difference between the car’s value and the loan balance, surrendering the car to repossession by the lender is an option as a last resort.

You’re probably familiar with involuntary repossession from TV shows. It can get ugly and uncomfortable for all involved. However, voluntary repossession is different. You simply make arrangements to hand over the vehicle to a representative of the lender who holds the lien on your vehicle. You’re not selling the car, so you’re not getting paid. But if you need a way out of your car loan and burdensome payments, it’s an option.

All repossession, including voluntary car repossession, will hurt your credit score. Your score will see a sharp hit immediately, and the even will remain on your credit report for up to 7 years. Make sure you understand how having a lower credit score could impact your future before following through with repossession.

Options For Keeping Your Car and Overcoming Negative Equity

1. Make Extra Payments on Your Loan

Consider paying extra each month toward the principal balance. Most auto loans do not have prepayment penalties in 2025, but it’s best to check with your lender to confirm. Making extra payments reduces your auto loan balance faster, closing the gap between what you owe and your car’s value.

Pros and cons of making extra car payments

Pros:

Reduces the loan balance quickly.

Avoids additional loans or rolling over debt.

Cons:

Requires extra financial resources.

Could take time, depending on the size of the negative equity.

2. Keep It Simple: Pay Off the Loan As Agreed

If you don’t need to sell or trade the car, the simplest option is to keep making payments until the loan is paid off or the car’s value exceeds the loan balance.

Depreciation is the root cause of most cases of negative equity. The good news is that depreciation slows tremendously after the first three years of vehicle ownership. If you can afford to keep making payments with your current loan, you will eventually be out of negative equity, guaranteed.

Pros:

Avoids additional loans or out-of-pocket expenses.

Builds equity over time.

Cons:

It may take years to resolve negative equity.

Depreciation could continue to outpace loan payments for some time.

How CarEdge Can Help

Navigating the complexities of negative equity and car buying doesn’t have to be stressful. With CarEdge’s free tools and expert services, you can make informed decisions:

👉 CarEdge Insights: Get real-time market data to understand your car’s value and local car market trends.

👉 Dealer Invoice Pricing: Negotiate the best price on your next car with this FREE tool.

👉 Car Buying Concierge: Let our experts handle every step of the buying, leasing, or selling process for you. Looking to get the most for your underwater trade-in? We can help!

Navigating the SUV market in 2025 can be a challenging endeavor, with fluctuating inventory levels and price trends that can make finding the right deal feel overwhelming. With so many options and so much money on the line, having the right information at your fingertips is invaluable. One crucial metric to consider is Market Day Supply (MDS).

MDS is a key indicator that measures how many days it would take to sell all available inventory at the current sales rate, assuming no additional stock is added. A high MDS would signal an oversupply of SUVs, which can give buyers more leverage to negotiate favorable terms. Conversely, a low MDS indicates limited availability, often leading to tougher negotiations in a seller’s market.

By leveraging CarEdge Insights, we’ve pinpointed which new SUVs are in abundant supply and which ones are harder to find in January 2025. Understanding these trends can empower you to make a more informed decision, whether you’re hunting for a compact crossover or a 3-row SUV.

Why does inventory matter to car buyers?

Inventory influences negotiability. When there’s a glut of cars, dealers will be more inclined to negotiate with you. Slim pickings? Not so much. This valuable insight can give you an edge in your car buying journey, helping you save money and avoid the hassle.

Here are the fastest and slowest-selling SUVs in America right now.

The Top 10 in January 2025: SUVs with the Highest Inventory

In January, a wide range of makes and models are represented in the top 10. What do they have in common? They’re mostly luxury models. The new Audi Q6 e-tron quattro takes the tip spot this month. Volkswagen Group’s EV sales have been slowing as competitors successfully take market share.

Alfa Romeo has two SUVs on the list. Both the Tonale and the Stelvio are slow-sellers in January. Another brand-new EV is high on the list this month – the 2025 Cadillac Escalade EQ. This nearly 9,000 pound EV is GM’s new flagship luxury SUV, but sales are slow to take off. Ford’s soon-to-be-discontinued Escape is the only mainstream model in the top 10 right now.

All of these slow sellers are especially negotiable. Don’t pay a dollar over MSRP for any of these SUVs!

The average selling price for the 10 slowest-selling SUVs is $74,201 in 2025.

Here are the 10 slowest-selling new SUVs, in other words, the models with the most inventory today.

The Bottom 10 in January 2025: SUVs with the Lowest Inventory

On the other side of the coin, these are the fastest-selling SUVs today. This month, we’re seeing the usual suspects on the list. Once again, Toyota dominates. Five of the ten fastest-selling new SUVs are Toyota or Lexus models.

BMW’s X3 and X5 are also quick sellers in January. The Chevrolet Traverse and GMC Yukon are also quick sellers. The Traverse has been revamped and improved for 2025, and it’s flying off the lots. The ultra-luxury Mercedes-Benz G-Class rounds out the bottom 10.

If you’re shopping for any of these new SUVs in 2025, you’ll be up against stiff competition. The average selling price for the 10 fastest-selling SUVs is $75,685. However, with the obvious outlier removed (the G-Class), the average selling price drops to $61,068.

See how much room there is to negotiate with the latest free tool from CarEdge – Dealer Invoice Pricing. Start your negotiations with confidence by using the dealer invoice price as your fair starting point.

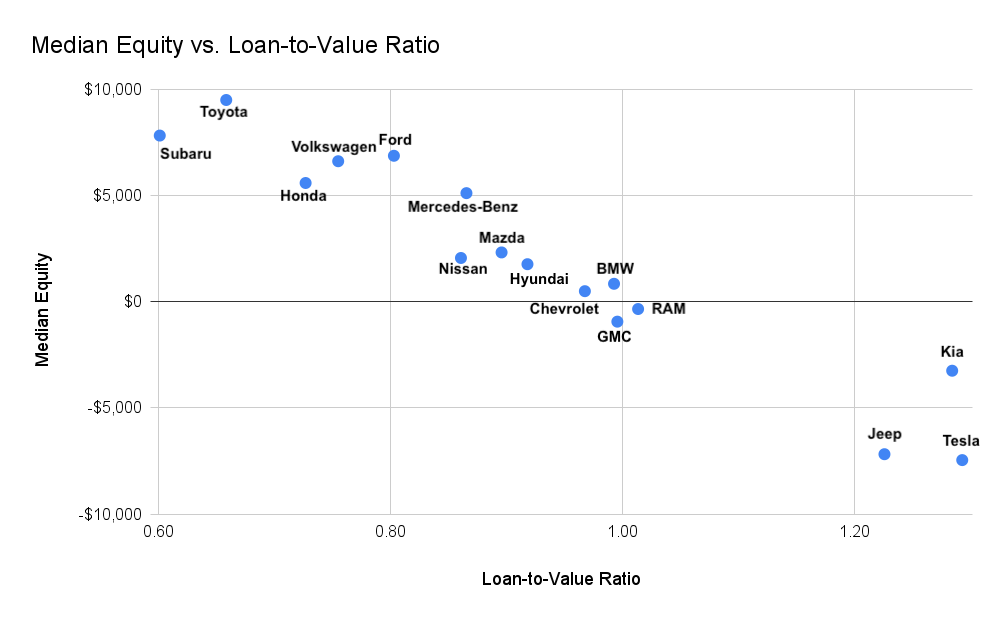

Negative equity, or owing more on a car loan than the vehicle’s market value, continues to rise as inflationary pressures and long loan terms take their toll on car buyers. CarEdge, in partnership with Black Book, surveyed 474 drivers in Q4 2024 to uncover the state of vehicle equity. Here are the highlights and the broader implications for drivers, car buyers, and the automotive industry.

In Q4 2024, 39% of drivers who financed their vehicles were underwater—up from 31% in Q3, a 25% jump. For cars purchased since 2022, the situation is even worse: 44% of these buyers owe more than their car is worth. As depreciation accelerates and long-term loans become the norm, the risk of negative equity continues to grow. This trend highlights a troubling financial burden on drivers and poses risks for the broader auto market.

Drivers Overestimate Their Car’s Value

Our survey reveals that 60% of drivers believe their car is worth more than its actual trade-in value. Of these, 18% overestimate by $5,000 or more, and 7% by over $10,000. This disconnect leads many to carry negative equity into their next car purchase, perpetuating financial strain.

When drivers attempt to trade in or sell their vehicles, they often face the harsh reality of lower-than-expected offers, which can derail their car-buying plans. Unfortunately, many choose to roll over the remaining debt into their next loan. This practice, while common, leads to higher monthly payments and extended loan terms, keeping buyers in a cycle of financial vulnerability.

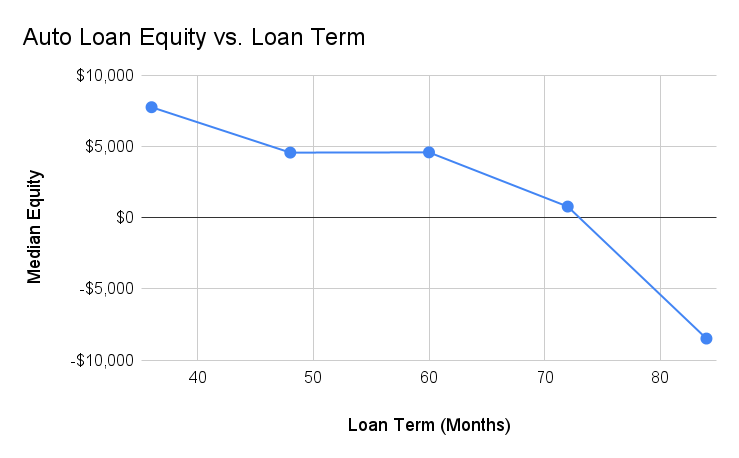

Long Loan Terms Drive Negative Equity

Loan terms significantly impact vehicle equity. Borrowers with 84-month loans face a median negative equity of -$8,485, while those with shorter 36-month terms have a positive median equity of $7,783. While longer loans make monthly payments more affordable, they also leave buyers trapped in equity-negative positions for years.

For many buyers, the appeal of lower monthly payments outweighs the long-term risks. However, as loan balances decrease more slowly with longer terms, these borrowers are more likely to face financial strain when attempting to sell or trade in their vehicles. Buyers who opt for shorter terms and make larger down payments tend to build equity more quickly, putting them in stronger financial positions.

EV Owners Are Most at Risk

Electric vehicle owners face the highest negative equity rates, with 54% underwater and a median equity of -$2,345. This makes EVs particularly vulnerable compared to gas and hybrid vehicles, which are more likely to have positive equity.

The rapid depreciation of EVs is a key driver of this trend. EV technology can become outdated quickly as newer models with improved range, charging speeds, and driver assistance features enter the market. Additionally, concerns about costly battery replacements and limited resale demand have led many buyers to prefer new EVs with warranties and a known history, further impacting the resale value of used EVs.

For EV buyers, understanding depreciation trends and factoring in long-term costs is critical to avoiding significant negative equity. Opting for shorter loan terms and considering potential incentives or tax credits can help offset some of the financial risks. Buyers who plan to hold on to their EVs for longer than just a few years are less likely to be impacted by negative equity with their auto loans.

What Does This Mean for 2025?

As we head into 2025, the issue of negative equity looms large for both consumers and the auto industry. For car buyers, rolling over negative equity into new loans can lead to long-term financial stress, reducing their purchasing power and limiting options. For the auto industry, high levels of negative equity could dampen trade-ins and slow new car sales, forcing automakers and dealerships to adjust their strategies.

Car dealers also face challenges when appraising trade-ins with negative equity. To close deals, dealers may need to discount new vehicles more aggressively or offer creative financing solutions, which can erode profit margins. Over time, high levels of negative equity in the market can disrupt the typical sales cycle

Navigating the Negative Equity Challenge

The Q4 2024 Negative Equity Report paints a clear picture of a growing issue in the car market. Drivers, car buyers, and the auto industry alike must address the challenges posed by rising negative equity.

CarEdge remains committed to empowering consumers with tools and insights to navigate today’s challenging car market. To avoid falling into the negative equity trap, car buyers should prioritize shorter loan terms, be familiar with expected car depreciation, and monitor used car values with tools like Black Book. Overcoming negative equity is possible when drivers make informed car buying and ownership decisions.

If you’re asking, “When is a good time to sell your car?”, the answer is almost always sooner rather than later. In general, your car is worth more today than it will be tomorrow. However, there are nuances for some drivers that can change the dynamic. Here’s a closer look at when selling makes the most sense, and when waiting won’t hurt.

2025 Is Almost Here

As the calendar approaches 2025, it’s important to recognize that your car’s value will drop significantly once the new year begins. On January 1st, your vehicle will effectively be considered a year older, even if it hasn’t aged by much in terms of mileage or condition. This is because most car buyers and dealerships use model year as a primary factor in determining value. If you’re thinking about selling or trading in your vehicle, now is the time to act before the new model year triggers additional depreciation.

Mileage plays a big role in determining a car’s resale value. Two critical thresholds where cars typically lose significant value are at 100,000 miles and 150,000 miles. Once a vehicle crosses 100,000 miles, it’s seen as a higher maintenance risk, which can reduce its value by up to 20%. At 150,000 miles, the depreciation steepens further, as buyers become wary of potential expensive repairs. If your car is approaching one of these milestones, it may be time to consider selling before the value drops significantly.

If You Don’t Sell Before Year’s End, Wait for Tax Refund Season

If you decide not to sell before the end of 2024, your next best option is to wait until the spring, when tax refund season fuels a surge in used car demand. Historically, many buyers use tax refunds to purchase used vehicles, making it an ideal time to sell and get a better price. As demand rises, so do resale values. Timing your sale around this season can help you maximize your car’s value.

How Hurricanes Impact the Used Car Market

Hurricanes Milton and Helene brought devastation to the Southeastern US in October. As the cleanup continues, the new and used car markets are beginning to feel the impacts. With a large number of vehicles damaged by flood waters and wind, thousands of cars were taken off of the market for the time being. This has created a spike in demand and pricing, which could work in favor of sellers. However, keep in mind that replacing your car during this shortage may be more expensive, and the risk of flooded cars on the market warrants caution for car buyers and sellers alike.

All-Wheel Drive Vehicles: Sell Before Winter Ends

For those owning all-wheel drive (AWD) vehicles, selling now is a strategic move. AWD cars and SUVs are highly desirable in cold climates, making this the season when demand (and therefore resale value) peaks. As winter fades and spring approaches, buyers become less interested in AWD vehicles, leading to lower offers. By timing your sale to match seasonal demand, you can justify a higher selling price, putting more money in your pocket.

In general, holding onto a vehicle means watching its value decline. When it comes to playing it smart, the rule of thumb is to sell when demand is high and before your car depreciates further. Stay informed about your car’s depreciation with theCarEdge Research Hub, where you can compare depreciation, total cost of ownership, and more to make an educated decision about your next move. It’s free data for all!

States eligibile for below invoice pricing and 100% free delivery:

Alabama, Arkansas, Texas, Oklahoma, Florida, Georgia, Kentucky, Louisiana, Maryland, Delaware, Mississippi, North Carolina, South Carolina, Tennessee, Virginia, and West Virginia.

What if I don’t live in these states? If you're outside these areas, don't worry! We're committed to making sure everyone can enjoy our deals. Although the delivery fee will not be waived, you can still purchase from CarEdge and either pay for shipping or coordinate pickup at a participating dealer.

Getting Started!

Please enter the following information to generate a price-transparent price quote.

FAQ

How much does it cost?

Our concierge service costs $999 plus an optional shipping fee (based on distance or pick-up).

To get started, pay the one-time payment of $999 and a CarEdge concierge will start by negotiating the vehicles in your favorites.

Why should you let a concierge do the work?

Get the best deal

Our team of concierges and industry experts with 75+ years of combined experience with access to tools and data to leverage the best deal possible.

Convenience

Gone are the days of looking for a car and stepping into the dealership spending hours and hours of head banging only to get smooth talked into a higher price.

Expert assistance

We answer all questions you may have regarding the buying process, what the right car is, the deal itself, and more!

Who are the concierges?

Transparent when others aren't

Our commitment to transparency and honesty ensures that you make informed decisions, while our years of experience guarantee that we will be able to secure the best deal for you.

When you win, we win

We work for you, not the dealership, ensuring your interests are always our top priority.

Buying a car just got a whole lot easier.

What happens next?

We’ll coach you on how to get dealers competing to get the best price

You’ll get instant access to our car buying checklists, guides, and market insights

What’s included in my car buying toolkit?

Dealer Invoice Price

Access the Dealer’s Invoice Price to negotiate an even better car deal.

Target Discount

A recommendation of for how much you should negotiate towards.

Negotiation Guide

Know exactly what you need to say to dealers to secure the best deal.

Exclusive Data

Info about your car such as cost of ownership, sales data, and more!

![Reviewed: 5 Best Instant Cash Offer Sites to Sell Your Car [2025]](https://stg-caredge-staging.kinsta.cloud/wp-content/uploads/2023/11/Image-1080x675.png)