Get access to the same vehicle valuation tool that dealers rely on. With Black Book, you’ll have insider data to accurately assess trade-in and purchase values—empowering you to negotiate the best possible deal.

It’s time to say goodbye to your old reliable car, but should you sell it privately or trade it in? Both options have their pros and cons, but with the right approach, you can minimize financial losses. Here are 10 tips to help you make the best decision.

10 Car-Selling Tips To Consider

1. Don’t name your price first

If a salesperson asks how much you want for your car, don’t give them a number. Let them make the first offer to avoid limiting your potential trade-in value. If asked, let them know that your primary interest is minimizing your net cost, or trade difference, after an allowance for your trade. Avoid providing any firm numbers, despite their repeated attempts to enquire, as they will be resolute in getting you to throw out the first number.

2. Tax benefits of trading in

Trading in your vehicle at the dealership can save you on sales tax. When you trade-in, you subtract the value of your car from the sales price of the new one, and you only pay sales tax on the difference in value. For example, if your trade-in is worth $20,000 and your state has a 5% tax, you could save $1,000 compared to selling it privately.

3. Don’t clean the car too early

If you’re just browsing, don’t clean out your car beforehand. A spotless trunk signals you’re ready to buy, potentially weakening your negotiation position.

4. Watch out for the higher offer trick

Dealerships may offer more for your trade-in but mark up the price of the new car. Don’t be fooled by the dealer that simply offers you the highest price for your car, as they may be getting you on the other side. Always look at the total cost.

5. Fix the obvious issues

If selling privately, get the obvious repairs fixed up front, and perform the routine service, like an oil and filter change. If your vehicle needs obvious repairs, private buyers will discount its value by at least 2X of the cost of the repair, as they will be concerned that it can’t be fixed, or that repairs will end up being more costly. Buyers don’t want to inherit a problem; they want a car that they can drive home with confidence, and is trouble-free.

6. Check your car’s history report

Run a vehicle history report before selling. Surprises on a report could deter buyers or lower your asking price. If you’re the original owner and have never had any problems or accidents, it’s possible to skip this step.

7. Organize vehicle documentation

Present your service records and manuals in an organized manner to instill buyer confidence. If you have them, make sure to include the vehicle registration, window sticker and any operating manuals that you received, so that you can present them to any possible buyer.

8. Trade where it makes sense

If your trade-in doesn’t match the dealership’s typical inventory, expect a lower offer. If you are at the BMW dealership, and you’re looking to trade in your 10 year-old Corolla with 120,000 miles, don’t expect a good offer. They won’t want your car, and will sell it straight to a wholesaler. Keep this in mind when thinking about a trade-in.

9. Meet in a public place

For safety, meet prospective buyers in public spaces like designated safe meeting zones rather than your home.

10. Pay off loans before selling

If possible, pay off any loans before selling. Having a clean title in hand, goes a long way towards resulting in a seamless transaction, versus having to get a bank involved. Sometimes banks will take weeks to send you a title that is free of liens, and that is enough to sour a lot of car deals. Similarly, make sure that you ask the private buyer how they intend to pay for the car.

Conclusion

Selling or trading your car doesn’t have to be stressful. By fixing minor issues, getting paperwork in order, and strategically timing your sale, you’ll increase your chances of getting a good offer. The more certainty you provide the buyer, the more they’ll be willing to pay. Learn more about resale values with CarEdge Research.

Did you know that depreciation makes up the biggest portion of the total cost of car ownership? When it comes to buying a new car, it’s important to consider how well it holds its value over time. Depreciation is the difference between the original sales price, and what the vehicle will be worth in the future. Some vehicles depreciate faster than others.

In this 2024 update, Toyota continues to dominate the list of cars with the best resale value, with multiple models making an appearance. Honda follows closely, proving once again that both brands know how to build cars that hold their value. Let’s take a look at the top contenders in terms of resale value in the first five years of ownership.

Jeep Wrangler

5-Year Residual Value: 75%

The Jeep Wrangler has long been known for its ability to retain value. After five years, it’s expected to depreciate just 34%, leaving you with a resale value of around $38,610 if you buy at today’s average selling price of $58,209. For off-road adventurers, the Wrangler’s value retention makes it a solid investment. See our full depreciation breakdown.

After a what feels like a lifetime, the 4Runner is getting a big refresh for 2025. We see no reason to worry about this legend’s reliability with the refresh, nor any damage to it’s phenomenal resale value.

Under normal ownership conditions, the Toyota 4Runner will depreciate just 39% after five years under normal use. With today’s average selling prices, this results in a resale value of about $31,593. If you’re looking for an SUV that holds its value while offering reliable performance, the 2025 4Runner should be on your short list. See our full depreciation breakdown.

The Land Cruiser is back after a short hiatus. As expensive cars sadly become the norm, it makes sense that Toyota would resurrect their luxury SUV with impressive off-road prowess. It’s quite expensive, especially for a Toyota. Today’s average selling price is a hair north of $73,000. After five years, the Land Cruiser retains 74% of its value, with an estimated resale price of $44,791. The time-tested Land Cruiser is a prime choice for anyone looking for a high-end SUV that keeps its value. See our full depreciation breakdown.

With a 5-year depreciation of just $10,127, the Toyota RAV4 is another excellent option for those looking for cars that hold their value. After five years, the average residual value will be around $27,520, making it one of the most practical choices for compact SUV buyers. See our full depreciation breakdown.

The Honda HR-V, the #3 crossover in America in terms of sales, retains 73% of its value after five years. Considering an average selling price of $29,164 when new, the average resale value after 5 years comes out to $21,266. It’s a great option for those who want a smaller SUV that still holds its value well. See our full depreciation breakdown.

The Honda CR-V is a top performer in the small SUV segment, losing just 28% of its value after five years. That leaves CR-V owners with an estimated resale value of $22,354 when starting at an average selling price of $38,461. The Honda CR-V is not just reliable; it’s a smart financial choice for those who care about SUV resale value. See our full depreciation breakdown.

They say it’s shockingly fun to drive considering the attainable price point. There’s yet another reason to love the Miata: low depreciation. The Mazda MX-5 Miata retains 72% of its value after five years, with an expected resale price of $23,885. Brand new, the MX-5 Miata sells for $36,239 on average as of 2024. Known for its sporty handling and fun driving experience, the Miata is one of the top choices for sports car buyers who also want excellent resale value. See our full depreciation breakdown.

The Toyota Tacoma is arguably the best pickup truck on the road for holding its value. After five years, it retains 72% of its value on average. That means after a new selling price averaging close to $47,000, buyers can expect a resale price of around $34,000 after five years. Its combination of reliability, durability, and value makes it a standout among mid-size trucks. See our full depreciation breakdown.

The Toyota Corolla proves that compact sedans can retain their value exceptionally well. With a 5-year depreciation of just 28%, a new Corolla purchased today is expected to retain 72% of its value. Its resale value, low cost of ownership and excellent fuel efficiency help the Corolla sedan survive the modern era’s shift to SUVs and crossovers. See our full depreciation breakdown.

No longer available as a sedan, the Impreza is officially a hatchback for 2024 and 2025. The Subaru Impreza holds onto 72% of its value after five years, with an expected resale price around $19,882. Subaru’s reputation for reliability and standard all-wheel drive make the Impreza a smart choice for those looking for value retention in a sedan that can handle every season. See our full depreciation breakdown.

When it comes to finding cars that hold their value, these cars, trucks, and SUVs are at the top of the list. Time and time again, Toyota and Honda continue to dominate. For 2024 and 2025, other brands like Subaru and Mazda also offer strong contenders for those who shop with resale value in mind.

Need help finding the perfect car with great resale value? Let CarEdge Concierge do the negotiating for you. We’ll help you find the best deals, negotiate the price, and even deliver your new car to your door. Learn more about CarEdge’s car buying service.

When buying an SUV, one thing you’ll want to keep in mind is depreciation. Some SUVs lose value faster than others, which can lead to a lower resale value when you’re ready to trade in or sell. With the consumer in mind, we’re highlighting five family-sized SUVs with the worst depreciation. Although depreciation may not be a dealbreaker, knowing what to expect before making your purchase is always smart. All data is based on the latest 2024 depreciation calculations from CarEdge. Not seeing the model your interest in? See all of our SUV depreciation data here.

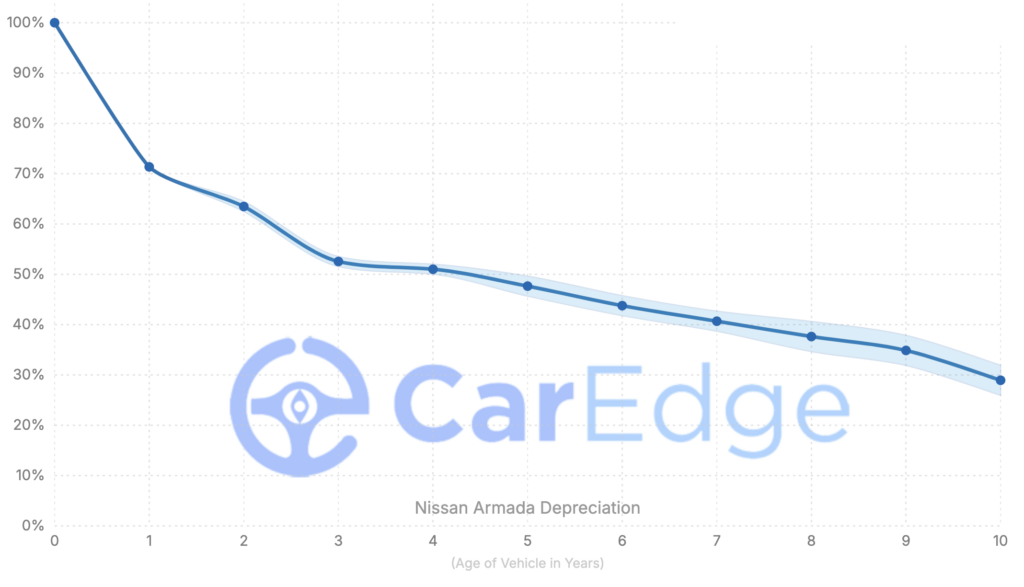

Nissan Armada: 52% Value Loss Over 5 Years

5-Year Residual Value: 48%

The Nissan Armada is a full-size SUV with plenty of space and power, but its value drops significantly after just five years. With a 52% depreciation rate, the Armada will have a resale value of around $32,604 after half a decade. For buyers, this could be something to consider, especially if you plan to resell or trade-in the vehicle later.

These depreciation numbers assume the vehicle is in good condition and has been driven an average of 12,000 miles per year. The average selling price for a new Armada is around $68,438.

The GMC Yukon XL is known for its room for the family, but it also has one of the highest SUV depreciation rates. After five years, the Yukon XL will lose around 52% of its value, with a resale price of approximately $42,083. This assumes the average selling price of $87,399, so the depreciation adds up to tens of thousands of dollars rather quickly.

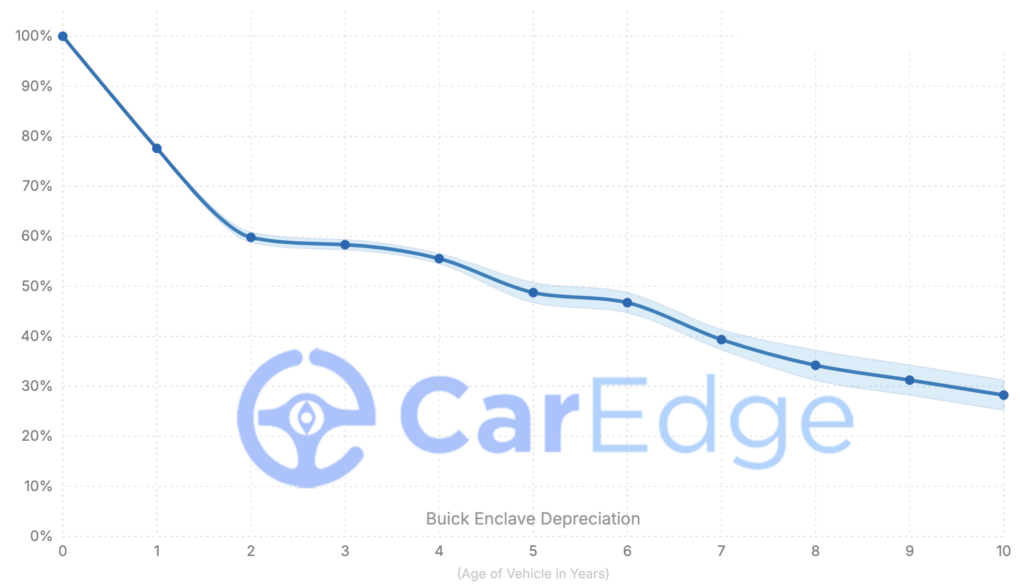

The Buick Enclave combines comfort and attainable luxury in a mid-size SUV package, but it comes with a significant depreciation cost. Today, the average selling price of a new Buick Enclave is $54,186. After five years, the Enclave will depreciate by about 51%, leaving it with a resale value of just $26,416. This might make you think twice, especially if selling your Enclave is a possibility in the next five years.

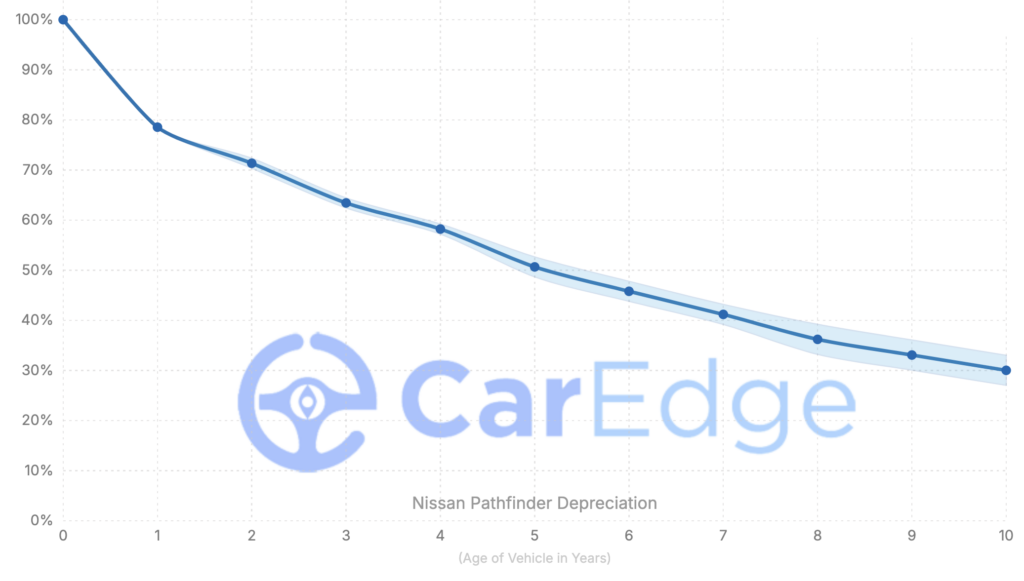

The Nissan Pathfinder is a legendary mid-size SUV, but it too suffers from a significant depreciation rate. After five years, expect a 49% loss in value, leaving you with a resale price of $23,921. The Pathfinder’s strengths remain, but the depreciation hit is worth keeping in mind.

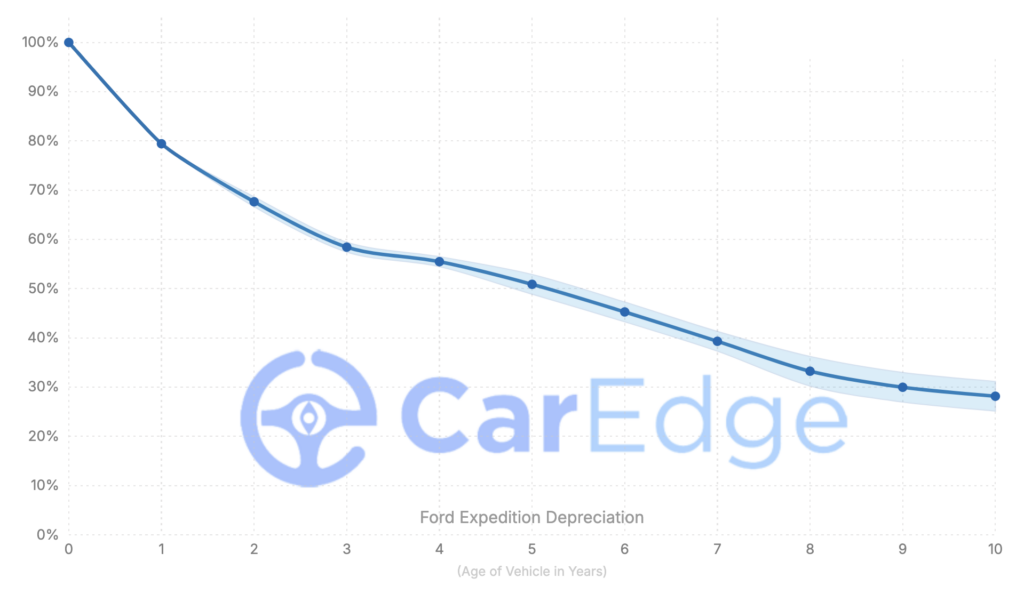

The Ford Expedition is one of the top three-row SUVs on sale, but it doesn’t hold onto its value as well as some might hope. After five years, the Expedition loses around 49% of its original value. While it’s packed with features, room for eight, and carries a solid reputation, the depreciation hit will cost buyers over $30,000 in resale value after just five years.

When shopping for an SUV, depreciation is a key factor that can greatly affect your long-term cost of ownership. The SUVs listed above have some of the worst depreciation rates in the market, meaning they lose significant value over time. If there’s even a small possibility that you could be selling in the next five years, depreciation should be a top factor in your decision making.

Want expert help to navigate your next SUV purchase? Let CarEdge Concierge do it for you. Whether you’re buying new or used, our team will negotiate the best deal for you and ensure you’re getting the most value for your money. Learn more about CarEdge’s car buying service.

Buying a truck is a costly endeavor, but not all trucks hold onto their value the same way. Some depreciate faster than others, leaving truck owners with less resale value down the road. In this deep dive, we’ll take a look at five trucks that don’t fare well when it comes to depreciation, so you know what to watch out for.

CarEdge’s depreciation rankings were updated with the latest data in 2024, giving you insights on which models are most likely to drop in value in 2025 and beyond. When we talk about “5-year residual values,” we’re referring to the percentage of a vehicle’s original value that it retains after five years. The higher the percentage, the better it holds its value—but for these trucks, the numbers aren’t looking too good.

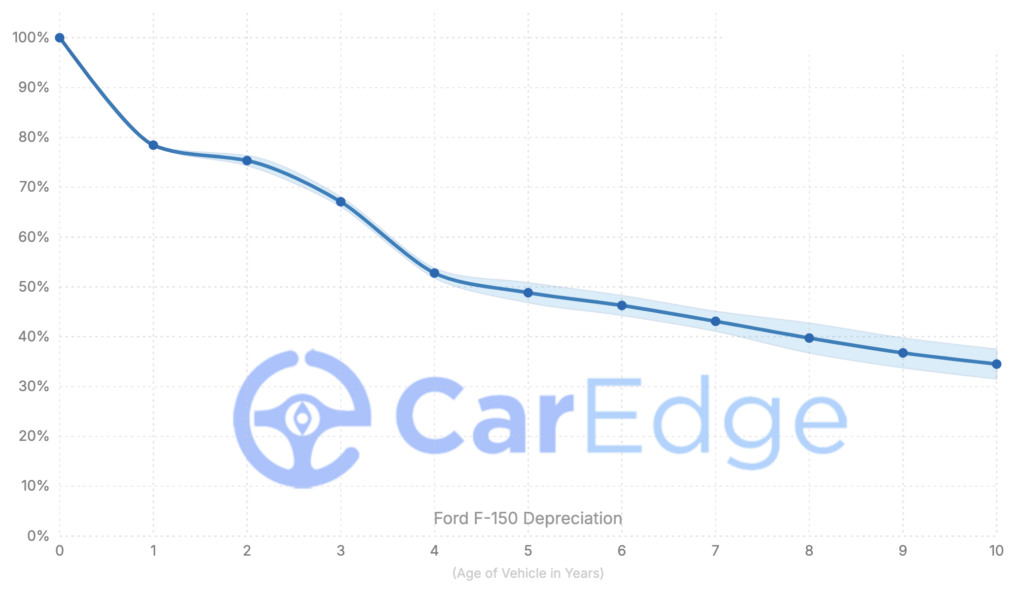

Ford F-150: 49% 5-Year Residual Value

The Ford F-150 might be a top-selling truck, but when it comes to value retention, it’s the worst. After five years, the F-150 will have lost around 51% of its original value, leaving you with a resale price of about $30,245. While it does well in the first few years, it starts to lag behind rivals like the Chevy Silverado as time goes on.

Should you avoid this truck? Not necessarily, but be aware of how fast it loses value. If you’re deciding between the F-150 and another truck, it might be worth considering factors other than just resale value, like features, towing capacity, or reliability. For instance, both the Chevy Silverado 1500 and Ram 1500 pickups maintain their value better than the F-150.

The chart above shows the expected depreciation for the next 10 years. These results are for vehicles in good condition, averaging 12,000 miles per year. It also assumes a selling price of $61,927 when new. This is the average selling price of a new F-150 today.” See our full depreciation analysis for the Ford F-150.

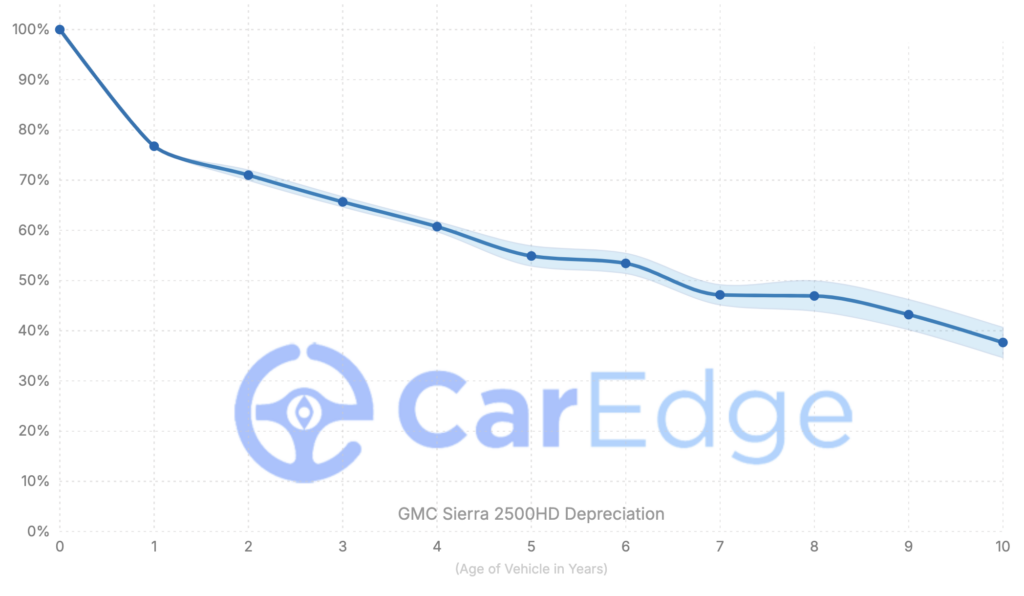

The GMC Sierra 2500 HD doesn’t depreciate quite as quickly as the F-150, but it still loses around 45% of its value over five years. If you buy one new at the current average selling price of $87,897, expect it to be worth around $48,247 after five years.

Heavy-duty trucks like the Sierra 2500 often fare better in the long run, thanks to their durability and strong market demand. But even with that in mind, a nearly 50% drop in value is something to keep in mind if you’re looking at this model.

The chart above shows the expected depreciation for the next 10 years. These results are for vehicles in good condition, averaging 12,000 miles per year. It also assumes a selling price of $87,897 when new. See our full depreciation analysis for the Sierra 2500.

Similar to the Sierra 2500, the Ford F-250 Super Duty retains just over half its value after five years. Starting at an average selling price of $72,489, it’s likely to be worth about $39,833 after that period. That’s a depreciation of $32,656, which isn’t insignificant for a heavy-duty truck.

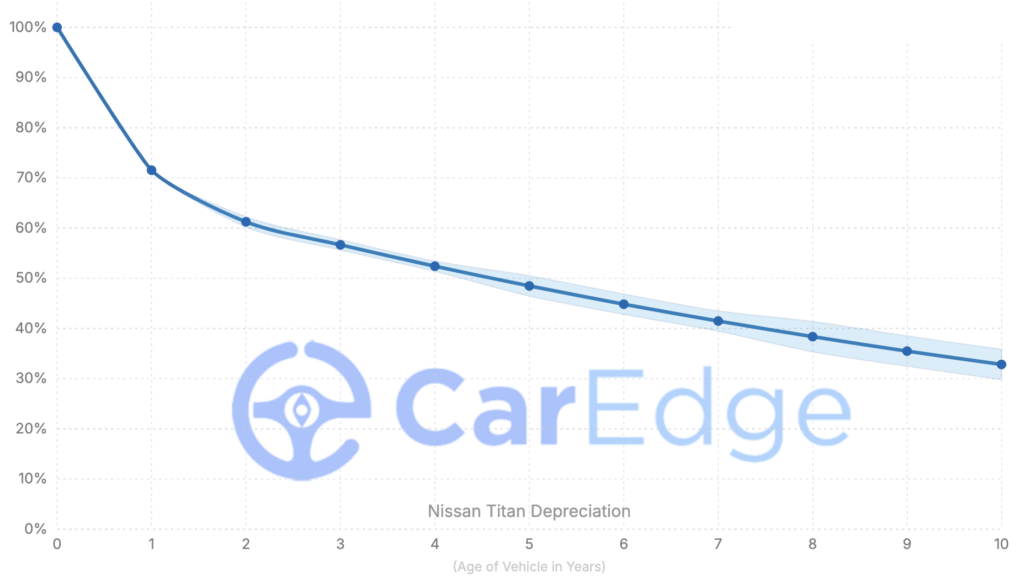

The Nissan Titan depreciates a bit more slowly than others on this list, but it’s still going to lose about 52% of its value in five years. From a starting price of $58,711, you’ll be looking at a resale value of around $28,463 after half a decade.

Nissan’s full-size truck may not be as popular as the F-150 or Silverado, but if you’re a fan of what it offers, be prepared for its resale value to dip more than average.

The chart above shows the expected depreciation for the next 10 years. These results are for vehicles in good condition, averaging 12,000 miles per year. See our full depreciation analysis for the Titan.

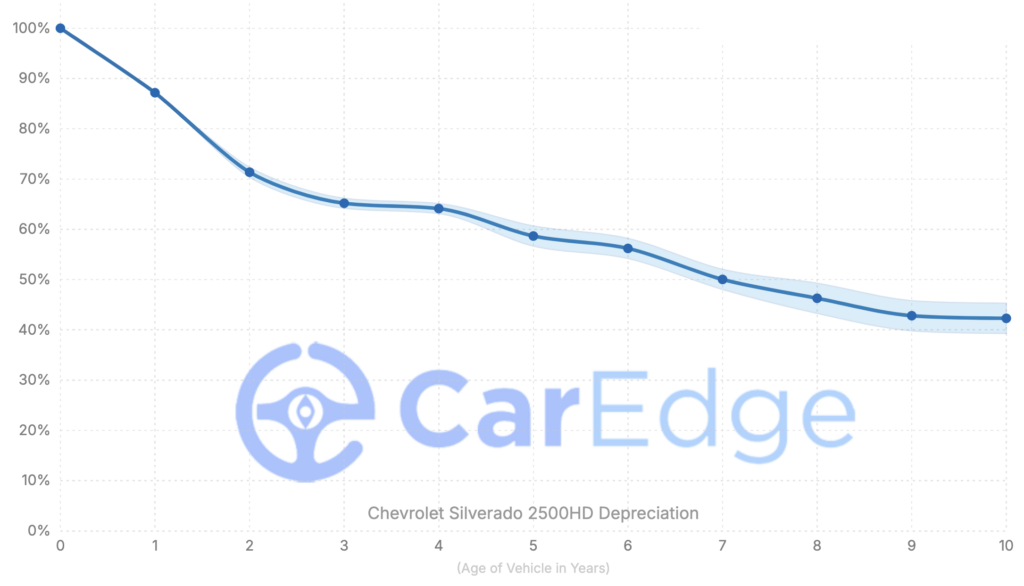

Chevrolet Silverado 2500 HD: 59% 5-Year Residual Value

The Chevy Silverado 2500 HD edges out the Titan with a 5-year residual value of 59%, meaning it loses 41% of its value over that time. If you purchase one for $66,710, expect it to be worth about $39,139 after five years.

It’s important to remember that these are the trucks with the worst depreciation. Several popular models fare better, including the Chevrolet Silverado 1500, GMC Sierra 1500, and trucks from Ram and Toyota. Browse our complete depreciation rankings for free.

In the market for a new or used truck? Let us do the negotiating for you. CarEdge Conciergeis the best-rating car buying service in America. Learn moreabout how we can deliver your next truck to your door, all while saving you thousands of dollars.

For many, there will eventually come a time when you need to part ways with a beloved car – even when you still owe money on it. Selling a car with an outstanding loan can seem daunting due to the added complexity of dealing with lenders. However, with a proper understanding of the process and careful planning, you can navigate the situation with ease. Here at CarEdge, we’re diving into how you can efficiently and effectively sell your car, even if the loan isn’t fully paid off yet.

Step One: Understanding Your Loan Details

When you’re considering selling a car that you still owe money on, the first crucial step is to fully understand the details of your loan. This knowledge is not only essential for setting the right sale price but also for ensuring that the transaction is handled legally and smoothly.

First thing’s first: understand your loan. That means digging up your login credentials to get into your online account with the lender. You may even need to give them a call, or hop on the live chat.

Here’s what to figure out before selling your car with a loan balance:

Check Your Loan Balance: Log in to your account, or contact your lender to request the current balance and the official payoff amount of your loan. The payoff amount may be higher than the balance due to the inclusion of any prepayment penalties or accrued interest.

Understand the Payoff Process: Ask your lender about the specific steps required to pay off the loan. You need to know how long it takes for them to process payments and release the lien. This timing is critical, especially if you need to coordinate with a buyer.

Lienholder Details: While your lender holds a lien on your vehicle, making them a key stakeholder, you don’t need their explicit permission to sell the car. However, you do need to pay off the loan. When you send the payoff check to your lender, include a signed payoff authorization form. This form authorizes the bank to send the lien release or the physical title directly to the new owner. By doing this, the buyer is protected, knowing that the necessary documents to prove ownership will be sent to them by the bank.

Obtain a 10-Day Payoff Quote: Most lenders will provide a quote that is valid for 10 days, which includes the total amount required to pay off your loan in full as of that date, including any additional fees or accumulated interest. This quote will be vital when you finalize the sale and need to settle the loan balance.

Step Two: Valuing Your Car

Next, determine how much your car is worth. Use trusted resources like Edmunds or Kelly Blue Book, and use CarEdge’s valuation tool to see how much online buyers will pay.

If you decide to go the private seller route, it’s important to price your car thoughtfully. Remember, you’re trying to sell the car quickly while also covering your remaining loan balance. Setting the right price can help you attract buyers quickly while ensuring you don’t fall short financially.

Step Three: Finding a Buyer

You have two main avenues for selling your car: a private sale or a dealership trade-in. A private sale typically yields a higher return but requires more effort on your part in terms of marketing and negotiation. Platforms like Facebook Marketplace, Cars.com, and AutoTrader are great for reaching potential buyers. On the other hand, trading in your car at a dealership is less hassle but is highly unlikely to offer as much for your car, especially with an outstanding loan.

With a dealership trade-in, it’s common to be offered 20-30% less than your car is worth in a private sale. If you could really use that additional money, going through the longer, more tedious process of selling privately may be worth it.

The financial aspect of selling a car with an outstanding loan can be tricky. But don’t give up now! If you’re eager to sell, it’s worth the hassle. Here’s how to handle it effectively:

Escrow Services: Using an escrow service for a private sale is strongly recommended as it adds a layer of security for both parties. The escrow service will hold the buyer’s payment until the loan is paid off and the lien is released, ensuring that the buyer doesn’t hand over money without securing the title, and you don’t transfer the title without clearing the loan.

Addressing Shortfalls: All payoff should be made with a cashiers check to further expedite the process. If the selling price doesn’t cover the loan payoff amount, you will need to provide the additional funds to clear the loan. Consider your options for covering this shortfall, such as a personal loan or a line of credit.

Payment to Lender: If you go this route, be sure to confirm that the buyer is comfortable with it before sealing the deal. It’s possible to coordinate with the buyer on making the payment directly to the lender. However, with a properly filled out payoff authorization stipulating that the documents go to the buyer, this would not be necessary.

Handling Overpayments: If the car sells for more than the payoff quote, plan how the surplus will be handled. Confirm with your escrow service (or with the buyer if they will pay your lender directly) to return the excess amount to you after the loan settlement.

Documentation: Keep meticulous records of all communications and transactions related to the loan payoff and car sale. Documentation should include the final payoff receipt from your lender and any agreements made with the buyer.

Step Five: Transfer of Ownership

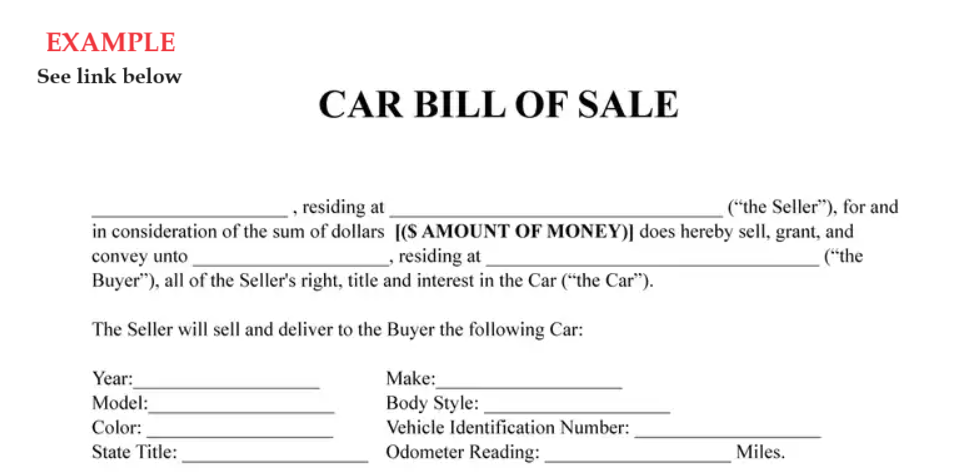

Transferring ownership involves a few small hurdles, but it’s nothing you can’t do! You must inform the buyer about the lien and ensure that the loan is fully paid before transferring the title. Even with a lien, you are legally required to provide the buyer with a bill of sale, documenting the transfer of ownership to the buyer. Alongside this, include a payoff authorization when you send the loan payoff to your lender. This authorizes them to release the lien or send the physical title directly to the new owner. Once you receive a lien release from your lender, you can complete the title transfer to the new owner.

Each state has different laws, so it’s important to check your local requirements. Check with your state DMV. The information should be easily found on their website.

If you want to avoid these hurdles, consider paying off the loan balance and securing the lien release before you sell the car. This approach eliminates many potential complications that could delay the sale.

Plan Ahead to Avoid Headaches (You’ve Got This!)

Selling a car with an outstanding loan requires careful attention to financial details and diligent record-keeping. With the right approach, you can sell your loan and transfer ownership without a hitch. Remember, knowledge is power in any transaction. Understanding how to handle this process can save you from potential financial pitfalls. For more insights and resources on managing car sales and ownership, keep it tuned to CarEdge.

👉 Want to become a car market pro? How about that and more for FREE?

Sign up for Deal School today, our free course for anyone interested in buying, selling, or simply owning a car the smart way.

Diving into the world of car ownership can lead you into murky waters, especially when grappling with negative car equity. Imagine owing more on your car loan than the vehicle is worth – a situation many Americans face today. This comprehensive guide illuminates the shadowy depths of negative equity: exploring its causes, the impact of recent economic trends, and, most importantly, effective strategies to steer clear of or manage it if you’re already caught in its grip.

Understanding Negative Equity: How It Happens

Negative equity, often described as being “upside-down” on a car loan, occurs when the loan balance surpasses the vehicle’s current market value. This financial quagmire can ensnare car owners due to:

Depreciation: Cars depreciate the moment they’re driven off the lot. If the loan repayment lags behind this depreciation rate, negative equity can develop.

Long-term Loans: Extending loan periods results in slower principal repayment, risking negative equity as cars depreciate faster than the loan diminishes.

Small Down Payments: Minimal initial down payments increase the financed amount, heightening negative equity risks if the car’s value rapidly decreases.

Rolling Over Loans: Incorporating remaining debt from a previous car into a new loan can immediately create negative equity.

Understanding these factors is key to avoiding or mitigating negative equity and ensuring a financially stable ownership experience.

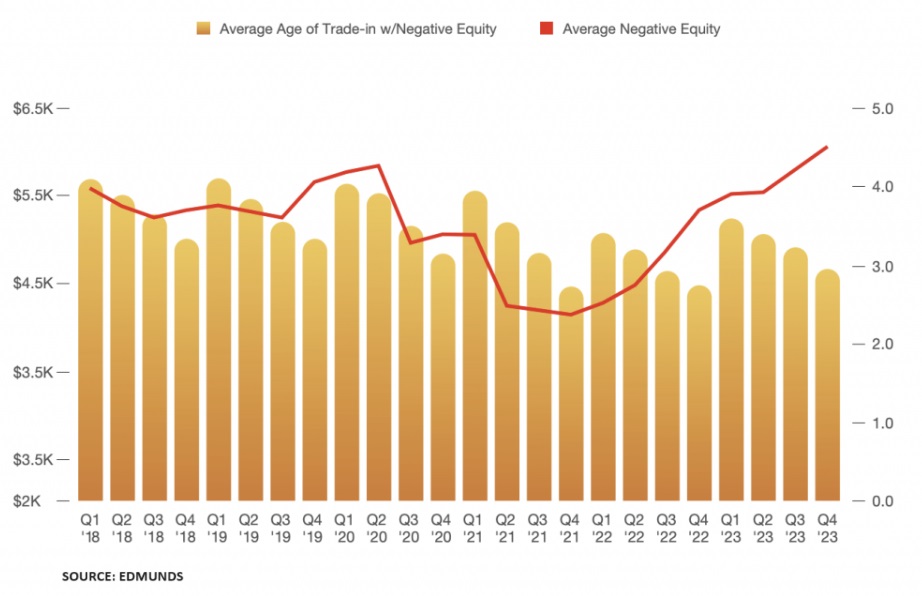

The Rise of Negative Equity in Car Loans

The phenomenon of negative car equity has been escalating, with recent Edmunds data revealing that 1 in 5 trade-ins have negative equity. The situation has become particularly pronounced in the new car market, where 20.4% of trade-ins are underwater, marking a significant jump from 14.9% in Q4 of 2021.

The average negative equity on car loans has surged to $6,054, setting a new record. This increase is partly attributed to the economic fluctuations during the pandemic when many consumers purchased vehicles at higher prices, leading to loans that exceeded the depreciating value of their cars. Consequently, drivers who bought cars during the pandemic are now facing the brunt of this financial imbalance.

What Negative Equity Means For You

Having negative equity on a car loan is more than just a numerical imbalance. It’s a predicament that can have lasting financial repercussions. Negative equity limits the owner’s flexibility, complicating efforts to sell or trade in the car without incurring losses.

For those looking to buy a new vehicle, negative equity means that the debt from the current car can roll over into the new loan. This leads to a cycle of increased debt that never seems to go away. Moreover, negative equity can affect credit scores and future loan conditions.

To combat these implications, car buyers should prioritize loan repayment strategies that target the principal amount. Also, consider shorter loan terms to align with the depreciation of the vehicle, and stay informed about the car’s current market value to make timely financial decisions. If you’d rather avoid the risk altogether, leasing is also an option.

Tackling Negative Equity

Navigating out of negative equity requires a proactive and strategic approach. Here are comprehensive steps and solutions to help you manage or eliminate negative car equity:

Accelerate Loan Repayment: One of the most straightforward methods to reduce negative equity is to make additional payments towards the loan’s principal. This will decrease the loan balance faster than the standard amortization schedule.

Refinancing the Loan: If you have good credit and interest rates have dropped since you took out your original loan, refinancing can be a smart option.

Consider a Shorter Loan Term: When refinancing, opting for a shorter loan term can result in higher monthly payments but will significantly reduce the interest cost and speed up equity building.

Lease a New Car: If you’re frequently facing negative equity with purchased vehicles, leasing might be a better option. Leasing a car can provide predictable monthly payments and eliminate the risk of negative equity, as you return the vehicle at the end of the lease term.

Cash-Injection on Trade-In: When looking to trade in a vehicle with negative equity, consider making a cash payment to cover the gap between the vehicle’s value and the loan balance. This can prevent the negative equity from rolling into the new loan.

Stay Informed About Your Car’s Value: Regularly check your vehicle’s current market value using tools like Sell With CarEdge, where you can receive multiple online offers at once. This awareness can help you make informed decisions about when to sell or trade-in the vehicle before the negative equity grows too large.

By employing these strategies, you can tackle negative equity head-on and work towards a more stable financial situation with your vehicle. Each approach has its considerations, so it’s important to evaluate your financial circumstances and car value carefully before deciding on the best course of action.

GAP (Guaranteed Asset Protection) insurance is indeed related to the topic of negative equity in car loans. Thus kind of insurance is designed to cover the difference between the actual cash value of a vehicle and the balance still owed on the financing (loan or lease) in the event that the car is totaled or stolen. Here’s how it connects to negative equity:

Protection Against Negative Equity: If a car is totaled or stolen, standard auto insurance policies usually cover only the current market value of the vehicle. If you owe more on your loan than the car is worth (negative equity), you would have to pay the difference out of pocket. GAP insurance covers this “gap,” preventing the financial strain of paying off a loan for a car you no longer possess.

Financial Safety Net: For car owners who are in negative equity, GAP insurance acts as a safety net, ensuring that they are not financially burdened by the remaining loan balance in case of total loss or theft of the vehicle.

Recommended for Long-Term Loans and Small Down Payments: For those who finance with long-term loans or small down payments, it’s smart to consider GAP insurance. It’s especially wise for leases and loans where the term extends beyond the standard three to four years.

In the context of managing negative equity, GAP insurance doesn’t reduce the loan balance or directly help in getting out of negative equity. However, it provides financial protection against the consequences of having negative equity in the event of an accident or theft.

Negative car equity, while daunting, is manageable with smart decisions and strategic actions. Understanding its roots and applying tailored strategies can lead car owners from the depths of financial strain to the clearer waters of financial stability and equity.

Want to learn more about how your particular situation may impact your ability to buy or sell? Chat with a CarEdge expert today. We’re here to help!

States eligibile for below invoice pricing and 100% free delivery:

Alabama, Arkansas, Texas, Oklahoma, Florida, Georgia, Kentucky, Louisiana, Maryland, Delaware, Mississippi, North Carolina, South Carolina, Tennessee, Virginia, and West Virginia.

What if I don’t live in these states? If you're outside these areas, don't worry! We're committed to making sure everyone can enjoy our deals. Although the delivery fee will not be waived, you can still purchase from CarEdge and either pay for shipping or coordinate pickup at a participating dealer.

Getting Started!

Please enter the following information to generate a price-transparent price quote.

FAQ

How much does it cost?

Our concierge service costs $999 plus an optional shipping fee (based on distance or pick-up).

To get started, pay the one-time payment of $999 and a CarEdge concierge will start by negotiating the vehicles in your favorites.

Why should you let a concierge do the work?

Get the best deal

Our team of concierges and industry experts with 75+ years of combined experience with access to tools and data to leverage the best deal possible.

Convenience

Gone are the days of looking for a car and stepping into the dealership spending hours and hours of head banging only to get smooth talked into a higher price.

Expert assistance

We answer all questions you may have regarding the buying process, what the right car is, the deal itself, and more!

Who are the concierges?

Transparent when others aren't

Our commitment to transparency and honesty ensures that you make informed decisions, while our years of experience guarantee that we will be able to secure the best deal for you.

When you win, we win

We work for you, not the dealership, ensuring your interests are always our top priority.

Buying a car just got a whole lot easier.

What happens next?

We’ll coach you on how to get dealers competing to get the best price

You’ll get instant access to our car buying checklists, guides, and market insights

What’s included in my car buying toolkit?

Dealer Invoice Price

Access the Dealer’s Invoice Price to negotiate an even better car deal.

Target Discount

A recommendation of for how much you should negotiate towards.

Negotiation Guide

Know exactly what you need to say to dealers to secure the best deal.

Exclusive Data

Info about your car such as cost of ownership, sales data, and more!