Get access to the same vehicle valuation tool that dealers rely on. With Black Book, you’ll have insider data to accurately assess trade-in and purchase values—empowering you to negotiate the best possible deal.

As manufacturers roll out year-end incentives, buyers are seeing more attractive offers for November 2024. From zero percent financing to cheap lease deals, there’s something for everyone. It’s worth pointing out that automakers update their incentives between the second and fifth business day of each month. Check back for updates this week!

The Best APR Offers In November

Low APR deals are growing in quantity and quality as we approach year-end sales. With interest rates officially falling, more deals are on the way. If you’re interested in any of these cars and trucks, what’s the use in waiting?

0% Financing! Chevrolet, Jeep, Nissan, and Mazda

In recent months, we’ve seen an increase zero percent financing. All of the following models are all advertised for 0% APR in November 2024.

JEEP – All Jeep models, from the Wrangler to the Grand Cherokee, have 0% APR for 36 months right now.

KIA – 2024 Kia EV9, EV6 (0% APR for 72 months). The slower-charging Niro EV is offered with 0% financing for 60 months. Kia is also offering the Sportage and Sorento at 0% APR for 48 months.

Ready to outsmart the dealerships? Download your 100% freecar buying cheat sheets today. From negotiating a deal to leasing a car the smart way, it’s all available for instant download. Get your cheat sheets today!

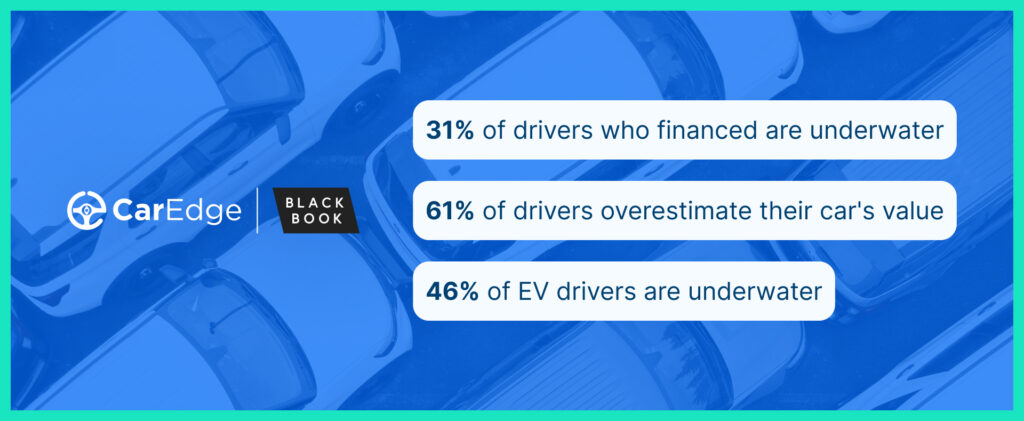

Negative equity, or being “underwater” on a car loan, is becoming a growing issue for many drivers in today’s market. As vehicle prices soar and depreciation accelerates, more car owners are finding themselves owing more on their loans than their cars are worth. CarEdge, in partnership with Black Book, surveyed nearly 1,000 drivers to understand the extent of this problem in Q3 2024. Here are the key findings.

According to our survey, 31% of drivers who financed their vehicles are currently in negative equity. This number rises to 39% for vehicles purchased since 2022, indicating that newer car buyers are especially vulnerable. As vehicle prices increase and long loan terms become more common, the risk of being underwater is higher than ever.

Most Drivers Overestimate Their Vehicle’s Value

A staggering 61% of surveyed drivers overestimate how much their cars are worth, with 17% believing their vehicle is worth at least $5,000 more than its true trade-in value. This disconnect can lead to unpleasant surprises when drivers try to trade in or sell their cars, often rolling over negative equity into their next auto loan and perpetuating the cycle.

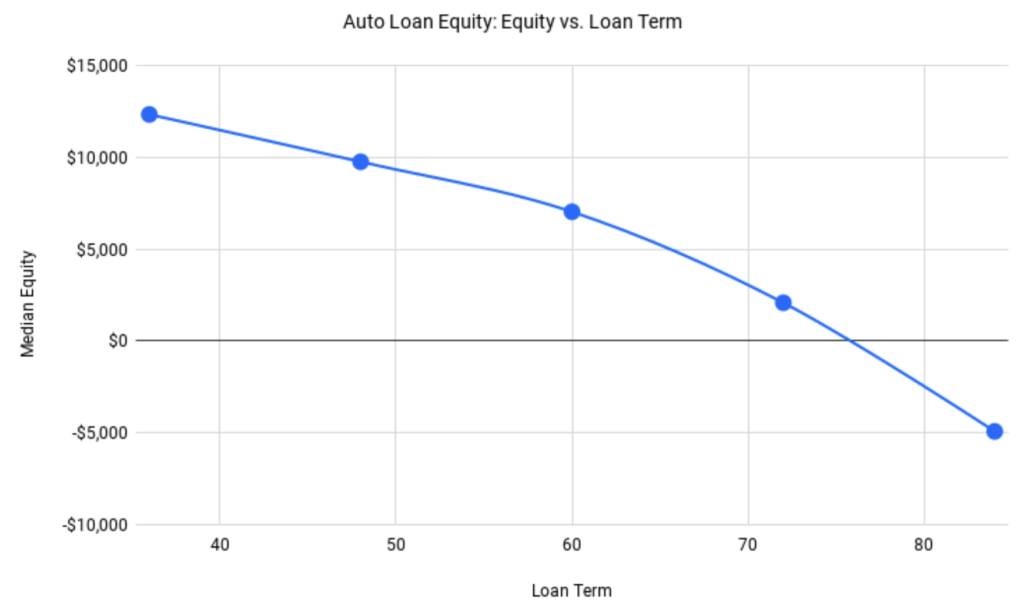

Longer Loan Terms Lead to Greater Negative Equity

Our data shows that loan terms directly impact vehicle equity. Car owners with 84-month loan terms are nearly $5,000 underwater on average, while those with 36-month loans typically have $12,340 in equity. Although longer loans reduce monthly payments, they also increase the likelihood of negative equity in the long term.

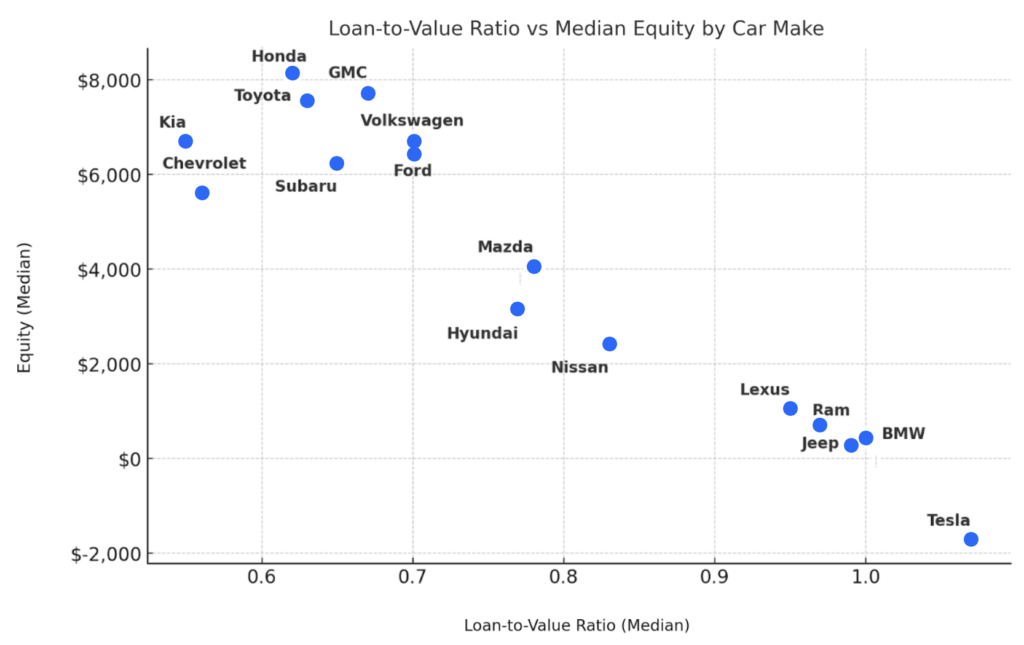

EV and Luxury Car Owners Are Hit Hardest

Electric vehicle owners are significantly more likely to be underwater. Of the EV owners we surveyed, 46% are currently in negative equity, with a median loan-to-value (LTV) ratio of 0.94—higher than the broader market’s 0.73. Luxury car brands like Tesla and BMW also see higher rates of negative equity compared to budget brands like Toyota and Honda.

A Concerning Trend for 2025

As more drivers find themselves underwater on their car loans, the negative equity issue is poised to become a major challenge for car owners and the auto industry alike. While budget car buyers may fare better, EV and luxury car owners are disproportionately affected.

CarEdge remains committed to providing insights and tools to help consumers navigate today’s car market. To learn more about vehicle equity and stay informed on auto news and market trends, visit CarEdge for expert analysis and guidance. For more information about Black Book’s industry-leading data and analytics, visit BlackBook.com.

As 2025 approaches, some car shoppers are finally seeing relief after years of price hikes. Several popular cars and trucks are getting price cuts in the new year. With automakers competing for U.S. market share and adapting to market demands, a few fan-favorites are over a thousand dollars cheaper for the new model year. Here’s a look at four crossovers and one popular pickup truck that are all receiving price cuts for 2025.

The 2025 model year is the last call for the Ford Escape. After two decades in the Ford lineup, the Escape will be discontinued to make way for EVs. As interest in the doomed crossover wanes, Ford has announced lower pricing for the 2025 model year. The popular Escape ST-Line is $1,500 cheaper for 2025.

When it comes to 2025 Ford Explorer pricing, trim options matter. Although the Explorer’s base MSRP increases by nearly $3,000, the more popular Explorer ST-Line gets $1,400 cheaper for 2025. Don’t pay a dollar over MSRP for this SUV!

Mazda sold over 70,000 CX-5s through the first half of 2024, but that’s not keeping them from launching an all-out price war with the crossover competition. For 2025, the Mazda CX-5 Premium Plus gets $1,300 cheaper.

Finally, more than a year after the Blazer EV arrived as a 2024 model, sales are starting to pick up. With a stop-sale for software issues well behind us, more drivers are scoring great deals on the sporty electric crossover. For the 2025 Blazer EV, GM is aiming to boost sales with a starting price that’s $1,200 lower.

The GMC Sierra 1500 is the only truck with falling prices for 2025. Even so, it’s hardly a discount. The popular AT4 spec is $300 cheaper for 2025. Not all trim options are seeing price cuts, but it’s worth mentioning due to rising prices for most of the full-size truck competition. However, seasoned truck buyers know that big cash and financing discounts are likely to arrive later in 2025 for those with patience.

With automakers slashing prices on some of the most popular models, 2025 is shaping up to be a better year for car shoppers. We recently shared our 2025 car market forecast, and we’d be shocked if more price cuts weren’t announced soon. Be sure to stay informed and explore the latest car offers with CarEdge, where you can find the best deals on these models near you.

If you’re looking for ways to save money on your car loan, refinancing could be the perfect solution. Whether falling interest rates have your attention or your credit score has improved, refinancing your loan can lower your monthly payments and reduce the amount of interest you’ll pay over time. This simple guide will walk you through the steps to refinance your car loan and help you decide if it’s the right move for you.

Refinance Your Car In 5 Easy Steps

Step One: Review Your Current Loan Terms

Before refinancing, it’s important to understand your current loan. Take a close look at your loan details, including the 1) remaining balance, 2) interest rate (APR), and 3) monthly payment.

You also want to check if your current loan has a prepayment penalty. Some lenders charge a fee if you pay off your loan early, which could impact whether refinancing saves you money. If you don’t see a prepayment penalty mentioned on your online banking portal, you may need to give your lender a call to find out.

Step Two: Review Your Financial Picture

To get a better auto loan rate, you’ll first want to check your FICO credit score for improvement. It’s best to check your credit score for free with the three major credit bureaus: Experian, TransUnion, and Equifax. It’s normal to see slight differences between your three major credit scores. To qualify for a better rate, you’ll need an improved credit score, and in most cases, proof of income. Once you’ve reviewed your credit score and overall financial picture, you’re ready to shop for rates.

Step Three: Shop For Better Rates

Refinancing is all about finding better terms. It’s smart to compare rates from multiple lenders, including banks, and credit unions. Even if you’ve always used one particular bank, you’ll want to review offers from other lenders. Compare offers from multiple refinancing lenders with CarEdge.

Keep in mind that different lenders may offer different terms, and the lowest interest rate isn’t always the best option. Look at the full loan package, including fees and repayment terms, to find the best deal for your financial situation. It’s also smart to see how much a better rate will save you using a free refinancing calculator.

Step Four: Apply For A Refinancing Loan

Once you’ve found the best refinancing offer, it’s time to apply for refinancing. Be ready to provide documentation such as your current loan details (including bank and account or loan number), proof of income, and information about your vehicle (VIN number, make, model, year, and mileage). Most lenders offer online applications, making the process quick and easy.

Step Five: Finalize Your Loan, And Rake In The Savings!

After your application is approved, your new lender will pay off your old loan, and your refinanced loan will take its place. From here, you’ll start making payments to your new lender at the lower rate. Be sure to set up auto-pay to ensure you never miss a payment on your new loan.

By refinancing, you’ll save money on interest and potentially lower your monthly payments, giving you more room in your budget. The process is simple, and the benefits can be huge over the long run.

As the Federal Reserve begins to lower interest rates for the first time in years, many car buyers are wondering when they’ll see relief in auto loan rates. While the Fed’s recent 50 basis point cut is a positive sign, the impact on auto loan rates may take a little longer to materialize. Here’s why consumers should be patient and what they can expect in the coming months.

Interest Rates Don’t Drop Overnight

The recent 50 basis point cut by the Federal Reserve has sparked hope for auto loan rates to go down, but the reality is that those rate reductions won’t happen overnight. Car shoppers can plan their purchase accordingly by understanding how car loan rates are expected to move in the weeks and months ahead.

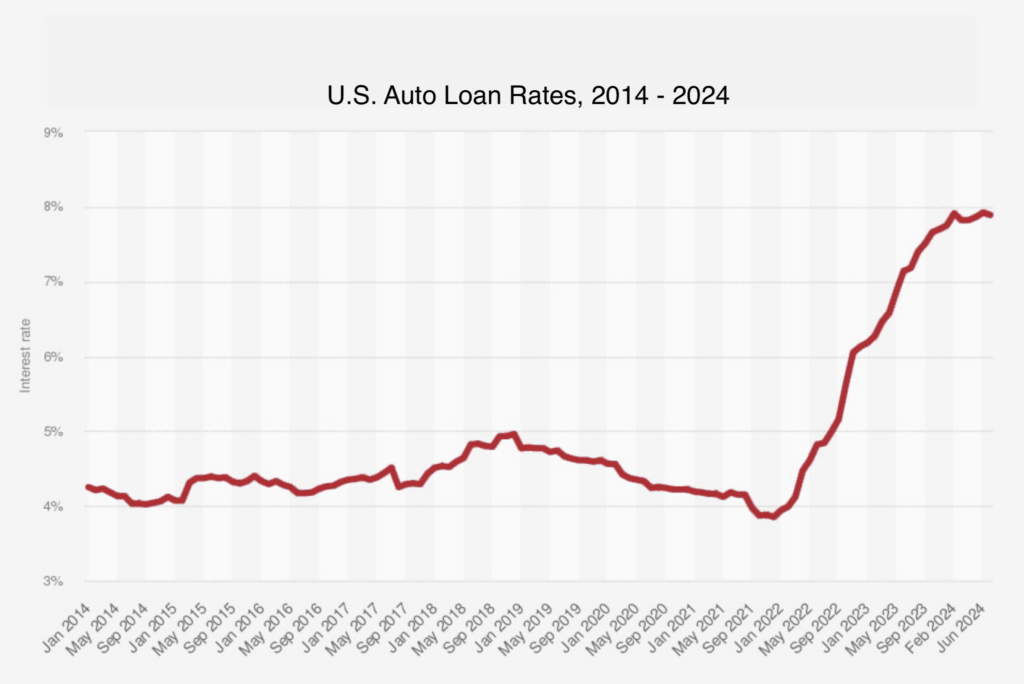

According to Cox Automotive, while the Fed’s interest rate cut marks the start of a broader easing cycle, it will take several weeks or even months for consumers to see significant drops in auto loan rates. The Fed doesn’t directly control auto loan rates, which are determined by market factors and lenders. In fact, auto loan rates tend to be “sticky” on the way down, meaning they’re slow to follow reductions in other market sectors, such as mortgage rates.

One key reason is that lenders are cautious about reducing the interest spreads on auto loans. Lenders continue to see shaky performance in the auto loan market, with higher delinquency rates and defaults. This makes lenders hesitant to lower rates too quickly. Auto loans represent a greater risk compared to other financial products, and lenders will wait to see sustained improvement in consumer financial behavior before they pass on lower rates to borrowers.

No sign of falling rates… yet

Cox Automotive notes that despite a decline in mortgage rates, auto loan rates have actually increased slightly in September. The average new car loan rate in September was 9.63%, while the average used car loan rate remained near recent highs at 13.95%. It may take several more weeks for car loan rates to slide downward.

Eventually, auto loan rates will go down, but consumers will likely see better deals on new vehicle financing first. Automakers work with ‘captive lenders’ to offer financing incentives. These banks are closely tied to the automaker. Captive finance companies are motivated to subsidize loan rates and drive sales.

As a result, we’ll see new car APR offers improving in the weeks ahead. As auto loan performance improves and credit spreads narrow, we’ll begin to see better rates for used cars, which have been hardest hit by recent increases in borrowing costs. It’s likely that the new year will arrive before used car loan rates fall significantly.

How Low Will Rates Go In 2025?

Most economists agree that rates won’t return to the lows we saw four years ago, when the Fed’s benchmark rates dropped to near zero. Instead, leading economists forecast a more realistic drop to the 3.00% to 3.50% range by the end of 2025. However, this forecast is subject to change if economic conditions worsen and the U.S. enters a recession, which could prompt the Fed to lower rates even further.

For car buyers, the path forward is clear. Car buyers looking for the lowest APRs should shop new car incentives. The average used car loan rate remains near multi-year highs, meaning drivers can save big by opting for new car incentives. Even today, new car offers often feature low-APR or even zero percent interest rates.

With year-end sales just around the corner, many automakers will offer aggressive financing deals to close out their oversupply of 2024 inventory. As we approach 2025, these deals are poised to get even better. Consumers who time their purchases right can maximize their savings.

Better Days Ahead

While auto loan rates won’t drop overnight, the upcoming months will bring better financing options for all car buyers. The Fed is on track to lower the benchmark rate several more times between now and late 2025. By late 2025, we could be looking at average APRs dropping below 6% for new car loans. Used car loans may finally fall back below 10% APR.

States eligibile for below invoice pricing and 100% free delivery:

Alabama, Arkansas, Texas, Oklahoma, Florida, Georgia, Kentucky, Louisiana, Maryland, Delaware, Mississippi, North Carolina, South Carolina, Tennessee, Virginia, and West Virginia.

What if I don’t live in these states? If you're outside these areas, don't worry! We're committed to making sure everyone can enjoy our deals. Although the delivery fee will not be waived, you can still purchase from CarEdge and either pay for shipping or coordinate pickup at a participating dealer.

Getting Started!

Please enter the following information to generate a price-transparent price quote.

FAQ

How much does it cost?

Our concierge service costs $999 plus an optional shipping fee (based on distance or pick-up).

To get started, pay the one-time payment of $999 and a CarEdge concierge will start by negotiating the vehicles in your favorites.

Why should you let a concierge do the work?

Get the best deal

Our team of concierges and industry experts with 75+ years of combined experience with access to tools and data to leverage the best deal possible.

Convenience

Gone are the days of looking for a car and stepping into the dealership spending hours and hours of head banging only to get smooth talked into a higher price.

Expert assistance

We answer all questions you may have regarding the buying process, what the right car is, the deal itself, and more!

Who are the concierges?

Transparent when others aren't

Our commitment to transparency and honesty ensures that you make informed decisions, while our years of experience guarantee that we will be able to secure the best deal for you.

When you win, we win

We work for you, not the dealership, ensuring your interests are always our top priority.

Buying a car just got a whole lot easier.

What happens next?

We’ll coach you on how to get dealers competing to get the best price

You’ll get instant access to our car buying checklists, guides, and market insights

What’s included in my car buying toolkit?

Dealer Invoice Price

Access the Dealer’s Invoice Price to negotiate an even better car deal.

Target Discount

A recommendation of for how much you should negotiate towards.

Negotiation Guide

Know exactly what you need to say to dealers to secure the best deal.

Exclusive Data

Info about your car such as cost of ownership, sales data, and more!