Get access to the same vehicle valuation tool that dealers rely on. With Black Book, you’ll have insider data to accurately assess trade-in and purchase values—empowering you to negotiate the best possible deal.

Buying a rental car can be an affordable way to get a newer vehicle, but it’s important to weigh the pros and cons. Rental cars are often priced lower than those privately owned, making them appealing to budget-conscious buyers. But are the risks worth it? Let’s weigh the pros and cons to find out.

Pros of Buying a Rental Car

Rental car companies like Hertz offer no-haggle prices on one to three-year old used cars, which can be significantly lower than the true market value. For example, a 2023 Tesla Model 3 could be thousands of dollars cheaper than its resale value. Additionally, rentals are well-maintained, with strict maintenance schedules and frequent cleanings. At least, that’s what’s supposed to happen. As many who have rented a car know, the experience can bring surprises, most notably unpleasant odors. With that said, let’s move on to the reasons why buying a rental car can be a bad idea.

Cons of Buying a Rental Car

While buying a rental car can save you money, it comes with some downsides. The most significant concern is high mileage. Rental cars often accumulate mileage faster than privately owned vehicles, leading to more wear on components. This is a big part of why rental cars are so affordable.

Additionally, while rental agencies maintain their fleets, cosmetic wear and tear from frequent use are not always addressed. Common signs of wear, like minor scratches or worn interiors, may still be present. Your rental car company should permit you to take the car to an independent mechanic for a pre-purchase inspection. These PPIs typically cost $100-$300, but it could easily identify problems that would cost you thousands of dollars.

Perhaps the most common complaint from those who rent cars is the smell. First, there are the lingering smells of previous drivers. Second, there are the odors that vehicle cleaning leaves behind. It’s not unusual to rent a car that somehow smells of cigarette smoke, even if smoking was never permitted in the vehicle. These odors can be very tough to eliminate.

Rental cars also tend to have limited features and are typically basic models without the higher-end trims or optional upgrades you might find in privately owned vehicles. Lastly, used car resale values may be lower than average, as many buyers shy away from purchasing former rental cars.

Buying an Electric Rental Car

With the rise of electric vehicles in rental fleets, buying an electric rental car can be a cost-effective option for those looking to make the switch on a budget. Hertz is selling thousands of EVs after learning that renters are hesitant to give EVs a try on a time-constrained business trip or vacation. After all, charging is time-consuming. However, there are some precautions that every used EV shopper should take, whether buying from a rental car company or elsewhere.

Consider the battery’s condition, as frequent short trips and rapid charging could reduce battery health. Don’t buy a used EV unless you can see what the estimated range is at 100% full charge, and compare the number to the EPA-rated range when new.

Always check the vehicle’s charging history to the best of your ability. If an EV was exclusively charged at DC fast chargers, it’s more likely to be in poor condition. Overnight ‘Level 2’ charging is easiest on high-voltage batteries.

Verify the battery warranty to ensure it’s still covered. Fortunately, EV battery and powertrain warranties typically last longer than coverage provided for ICE vehicles. See the best (and worst) EV battery warranties.

Final Thoughts: Consider Your Wants, Needs, and Budget

Buying a rental car can be a cost-effective way to get a reliable vehicle, but it’s essential to weigh the pros and cons. High mileage, potential cosmetic wear, and limited features may not matter if your primary goal is affordability and ease of purchase. However, you should always get a vehicle history report and inspect the car carefully. If you’re looking for an affordable car without the frills, a rental car could be a smart choice. For EV shoppers, pay extra attention to battery health and charging history to ensure you’re getting a well-maintained vehicle.

See depreciation data, total cost of ownership, maintenance costs, and so much more at the 100% FREE CarEdge Research Hub.

Buying a car from a private seller can be tempting, especially when the price is right. But private sales come with risks that you need to be aware of before making a deal. Unlike dealerships, private sellers don’t have the same accountability, making it crucial for buyers to do their homework. Here are some important risks to consider when buying a vehicle through a private sale.

1. Sellers May Not Always Be Transparent

While dealerships rely on reputation, private sellers often aren’t as concerned about being 100% truthful. There’s little downside for them to leave out important details about the car’s condition, especially if it means losing money. That’s why it’s essential to approach private sales cautiously and assume the seller might not disclose everything. Always request a vehicle history report to get the facts.

2. Hidden Liens on the Vehicle

One of the biggest risks when buying from a private seller is the potential for hidden liens on the vehicle. If there’s unpaid work or debts associated with the car, the new owner becomes responsible for them. A vehicle history report should help disclose any liens or outstanding debts, so make sure you check before purchasing. A hidden lien is rare, but a huge pain if it happens.

3. Undisclosed Mechanical Problems

Private sellers may list their cars for sale after a dealer refuses to accept it as a trade-in, often due to mechanical issues. These problems may not be immediately obvious without professional diagnostic equipment. To protect yourself, always have the car inspected by a trusted mechanic before finalizing the sale. Learn more about Pre-Purchase Inspections.

4. Vehicle History Reports Aren’t Foolproof

While vehicle history reports provide valuable insight into a car’s past, they only contain what’s been reported. If an accident wasn’t documented, it won’t show up on the report. To avoid surprises, have a professional pre-purchase inspection check for signs of damage, such as mismatched paint or replaced body panels.

5. State Inspection Issues

Each state has different safety and emissions standards, and just because a car passes inspection in one state doesn’t mean it will pass in another. Things like window tinting, ground clearance, or other modifications can become costly issues. Make sure the car meets your state’s requirements before making a purchase. If you live in a state with strict inspection criteria, buying a used car, especially an older car, will involve a higher risk of a failed state inspection, and the need for costly repairs.

6. Limited Recourse with Private Sales

Unlike dealerships, private sellers aren’t subject to the same regulations and oversight. If something goes wrong after the sale, your options for recourse are limited. Legal action against a private seller can be costly and time-consuming, leaving you with few alternatives if the car turns out to be less than advertised.

How to Protect Yourself in a Private Sale

If you’re considering buying a car from a private seller, take steps to protect yourself. Obtain a vehicle history report, research expected resale values, and get a mechanic’s inspection. These steps will help ensure that you’re making a smart decision and not getting stuck with a vehicle that could end up costing you more in the long run. But here’s the bottom line: unless you personally know the seller and have a high amount of trust in them, it’s impossible to be 100% certain that you are avoiding the risks mentioned here.

Check out the following video for more information on today’s used car market:

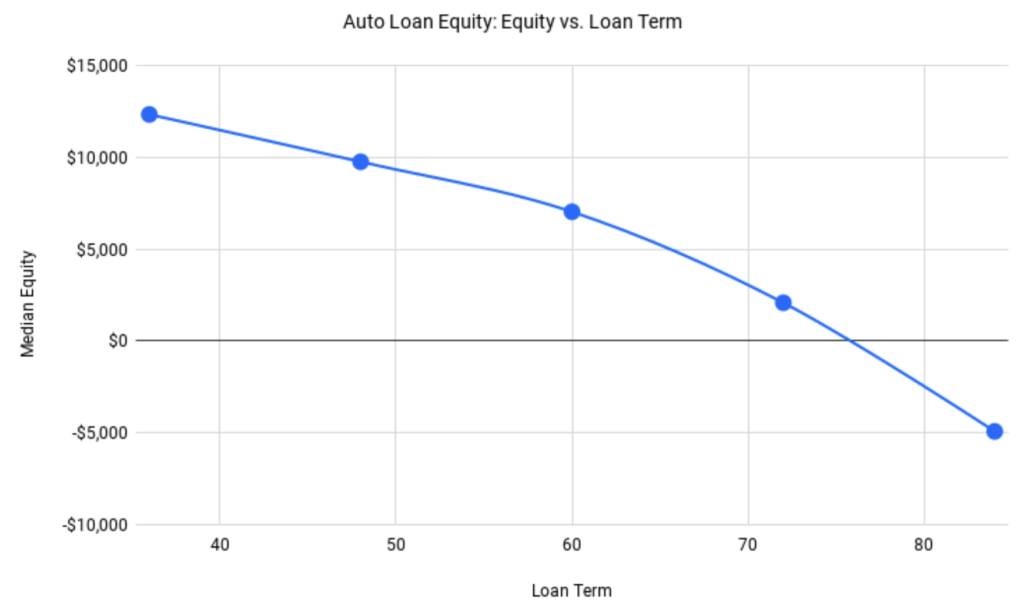

As car prices remain high, many buyers are opting for longer car loans to keep their monthly payments manageable. According to new data from Edmunds, 84-month loans are on the rise. In fact, 84-month car loans have grown from 15.8% of new loans in Q1 2024 to 18.1% in Q3 2024. The average car loan term is now 68.8 months, remaining near all-time highs.

While these extended loan terms might lower monthly payments, they come with serious risks that could impact your finances for years to come. Here’s what you need to know, and how to play it smart when financing your car.

1 in 3 Drivers Have Underwater Car Loans

84-month loan terms are becoming popular, but that doesn’t mean they’re a good idea. In fact, far from it. As auto loan rates begin to fall, more car buyers are warming up to the idea of longer loan terms. This is a bad sign of things to come in 2025, unless consumers begin to think-twice about extending auto loans.

Our Q3 2024 CarEdge Negative Equity Report shows that 31% of drivers who financed their vehicle are underwater on their loans. The situation is worse for those with loans longer than 60 months, especially 84-month terms, which lead to slower equity growth and higher chances of negative equity. Among the survey respondents with 84-month loan terms, an astounding 71% are underwater. Clearly, longer loan terms increase the likelihood of negative equity for car owners.

One of the main reasons for this is depreciation. With long loan terms, cars lose value faster than the loan is paid off, leaving borrowers owing more than their vehicle is worth. With a longer loan, the gap between loan balance and vehicle value grows wider, putting drivers in a financially vulnerable position.

Why You Should Avoid 84-Month Loans:

Negative Equity Risk: Longer loans increase the likelihood of being underwater, especially as depreciation outpaces loan payments.

Higher Interest Costs: Even with a lower monthly payment, you’ll end up paying more in interest over time.

Limited Flexibility: Being stuck in a long loan makes it harder to trade in or sell the car, especially if you’re upside down on the loan.

Smart Car Buying Tips:

Opt for a loan term no longer than 60 months to build equity faster.

Consider saving for a larger down payment to reduce the loan amount.

Shop for the best interest rates and avoid stretching your budget just to lower monthly payments.

Protect Yourself From Long-Term Financial Risks

While the allure of lower monthly payments with an 84-month loan can be tempting, the long-term risks far outweigh the benefits. Negative equity, higher interest costs, and lack of financial flexibility are all too common with extended loan terms. To protect your financial future, it’s smart to opt for shorter loan terms, build equity faster, and avoid stretching your budget just to secure a lower payment.

For more in-depth information on auto depreciation, maintenance costs, and total cost of ownership for hundreds of models, visit theCarEdge Research Hub. It’s 100% free!

Fall is underway, and better truck deals are here. With 2025 models arriving daily and dealers eager to sell remaining 2024 inventory, it’s a great time for negotiating, or letting us do it for you. Here’s our guide to the top truck deals of October 2024, featuring low APR financing, cash offers, and lease deals.

Automakers release their deals between the first and fifth of each month, so check back soon for the latest.

2024 Nissan Titan

Starting MSRP: $40,350+

Negotiability Score: Very High (141 days of market supply)

0% APR financing for 60 months

Nissan is fighting hard for truck market share in the U.S., with limited success. Today’s zero percent financing offer is the best truck deal today at 60 months. This offer expires on 11/02/2024.

Negotiability Score: High (181 days of market supply)

2024 Ram 1500 and 2024 Ram 1500 Classic: 0.9% APR for 72 months

Ram trucks are slow-selling, even though they seem to be everywhere you look on the road. To alleviate Ram’s oversupply of trucks, they’re offering huge financing offers this month. This offer expires on 11/02/2024.

Negotiability Score: High (112 days of market supply)

0% APR for 36 months + NO payments for 90 days, or lease for $409/month for 36 months with $4,949 due

With 112 days of market supply, there’s an abundance of 2024 Silverado 1500s on Chevy dealer lots. These APR and lease offers are great deals for truck fans. This offer expires on 11/02/2024.

Download your 100% freecar buying cheat sheets today. From negotiating a deal to leasing the smart way, it’s all available for instant download. Ready to let a car buying pro take the wheel?CarEdge Concierge is the easiest way to buy a car today. Our team finds the vehicle you want, right down to the finest of details, and negotiates on your behalf. Home delivery is available. Learn more about CarEdge’s car buying service.

Looking to get into a new vehicle for the least amount of money possible? We’re here to help. Despite new car prices remaining near record highs in March, affordable lease options remain as automakers look to move inventory. Surprisingly, there are several new car leases under $200/month. Bump your budget up to $250/month, and you have plenty to choose from. From sedans to EVs and popular crossover SUVs, these are the cheapest lease deals for March 2025.

Important note: The following advertised manufacturer offers exclude taxes, title, and fees. The dealer sets the final price. Automakers announce new monthly sales between the second and fifth of each month.

Whether you prioritize fuel efficiency, space, or the latest technology, the cheapest lease deals prove that you can have it all. Remember to act quickly, as these deals expire at the end of the month.

Ready to skip the BS and lease the easy way? Do it all from the comfort of home with CarEdge. With home delivery available (free in select areas) and our famous pre-negotiated pricing, we’ll simply deliver the car you want to your door.

States eligibile for below invoice pricing and 100% free delivery:

Alabama, Arkansas, Texas, Oklahoma, Florida, Georgia, Kentucky, Louisiana, Maryland, Delaware, Mississippi, North Carolina, South Carolina, Tennessee, Virginia, and West Virginia.

What if I don’t live in these states? If you're outside these areas, don't worry! We're committed to making sure everyone can enjoy our deals. Although the delivery fee will not be waived, you can still purchase from CarEdge and either pay for shipping or coordinate pickup at a participating dealer.

Getting Started!

Please enter the following information to generate a price-transparent price quote.

FAQ

How much does it cost?

Our concierge service costs $999 plus an optional shipping fee (based on distance or pick-up).

To get started, pay the one-time payment of $999 and a CarEdge concierge will start by negotiating the vehicles in your favorites.

Why should you let a concierge do the work?

Get the best deal

Our team of concierges and industry experts with 75+ years of combined experience with access to tools and data to leverage the best deal possible.

Convenience

Gone are the days of looking for a car and stepping into the dealership spending hours and hours of head banging only to get smooth talked into a higher price.

Expert assistance

We answer all questions you may have regarding the buying process, what the right car is, the deal itself, and more!

Who are the concierges?

Transparent when others aren't

Our commitment to transparency and honesty ensures that you make informed decisions, while our years of experience guarantee that we will be able to secure the best deal for you.

When you win, we win

We work for you, not the dealership, ensuring your interests are always our top priority.

Buying a car just got a whole lot easier.

What happens next?

We’ll coach you on how to get dealers competing to get the best price

You’ll get instant access to our car buying checklists, guides, and market insights

What’s included in my car buying toolkit?

Dealer Invoice Price

Access the Dealer’s Invoice Price to negotiate an even better car deal.

Target Discount

A recommendation of for how much you should negotiate towards.

Negotiation Guide

Know exactly what you need to say to dealers to secure the best deal.

Exclusive Data

Info about your car such as cost of ownership, sales data, and more!