Get access to the same vehicle valuation tool that dealers rely on. With Black Book, you’ll have insider data to accurately assess trade-in and purchase values—empowering you to negotiate the best possible deal.

In a startling turn of events, Reuters reports that Tesla has abandoned its plans to launch a $25,000 electric vehicle, a project that is integral to the company’s strategy for making electric vehicles more accessible and expanding its EV market domination. This move has sent ripples through the auto industry and financial markets. Here’s what we know about this developing story.

Update: Multiple outlets are reporting that Tesla CEO Elon Musk has responded to Reuter’s report, refuting the claims made in the article. More updates to come!

Reuters: Development of the Tesla Model 2 Halted

According to breaking news reported by Reuters, the word among Tesla leadership is that all work on the $25,000 Tesla in development is halted, effective immediately. Tesla had previously indicated in January that production of the affordable model, often referred to as the Model 2, would commence at its Texas factory in the second half of 2025.

However, the company is now shifting its focus towards developing robotaxis, despite the greater engineering and regulatory challenges this entails. This pivot was revealed in a late February meeting attended by numerous Tesla employees, where Elon Musk’s directive to prioritize robotaxis was communicated.

The decision to cancel the Model 2 project has left industry analysts questioning Tesla’s ability to meet its ambitious sales targets. Elon Musk had aspired for Tesla to sell 20 million vehicles by 2030, a goal that now seems more elusive with the affordable car’s cancellation.

The company’s current cheapest model, the rear-wheel drive Model 3 sedan, is priced at around $39,000 in the U.S., well above the intended price point of the Model 2. Federal tax credits have contributed to Tesla’s sales growth, but have been reduced or eliminated for some Tesla models in recent months.

Chinese EVs a Looming Threat

Tesla’s shift in strategy comes amid intense competition, particularly from Chinese electric vehicle manufacturers who have successfully entered the market with significantly lower-priced models. This competitive pressure appears to have influenced Tesla’s strategic redirection.

The move comes less than a week after Tesla began a ‘free’ Full Self-Driving trial for all Tesla drivers with capable hardware. It remains to be seen if Tesla’s biggest FSD promo to date will drive conversions towards the $12,000 add-on.

As Tesla discontinues its plans for the Model 2, the company’s focus on robotaxis and high-end models like the Cybertruck continues. However, this approach has raised concerns about Tesla’s market positioning and long-term profitability, given the rapid growth and pricing strategies of competitors, particularly in the burgeoning electric vehicle market in China.

This development is a significant deviation from Tesla’s long-standing goal of making electric vehicles more affordable and widely accessible, a vision that has been central to its brand and business model. The cancellation of the affordable Tesla model and the company’s recalibrated focus on robotaxis and higher-end vehicles mark a critical juncture in its journey, with potential implications for its competitive edge and market share.

As Tesla navigates these strategic shifts and market dynamics, the automotive industry and investors are keenly watching to see how these changes will affect the company’s trajectory and the broader electric vehicle landscape. This is a developing story, and further updates are anticipated as more information becomes available.

As new cars fill dealership lots, OEMs are lowering prices to sell cars. From Jeep to Ford, and even Mazda’s new flagship SUV, price drops have already arrived. However, as we’re about to see, there are several other models that are in desperate need of MSRP reductions given today’s oversupply and weak sales. Don’t pay a dollar over MSRP for these new cars, trucks, and SUVs that are primed for price cuts in 2024. Especially when you have the power of CarEdge Insights at your fingertips.

Let’s dive into the details.

Nissan Altima: The Sunset of a Sedan

Base MSRP: $27,140

Average Selling Price: $30,463

Current Market Day Supply: 198 days

After decades leading Nissan sales forward, the Altima will be discontinued in 2025. It’s true that the Altima has become the butt of jokes in car culture in recent times, but its absence will be immediately felt by those who simply need an affordable ride.

But Nissan has its reasons. Altima sales have been in decline, dropping 8.5% in 2023 while most of the rest of Nissan’s lineup saw modest gains. There remains a 198-day supply in America today. With the looming discontinuation on the horizon, it’s prime time for a price drop.

The Dodge Hornet is facing a surplus, with the third-highest inventory among all new cars as of April 2024. This equates to nearly two years of supply if production were to cease today.

Why are buyers balking at the Hornet? For one thing, there are 4 recalls for the Hornet as of early 2024. Consumer Reports rates it at 55 out of 100 overall, with average reliability but above-average owner satisfaction scores. However, it’s full of compromises, too many perhaps. It’s not as spacious as competing crossovers, but it’s bigger than a sedan. Fuel economy is among the worst in the compact crossover segment at 24 miles per gallon in combined driving. There is a plug-in hybrid version that fares much better.

Jeep’s Grand Wagoneer, despite being the brand’s priciest model, is overdue for a price cut. Jeep has already reduced prices on other models in 2024, from the Wrangler to the Gladiator.

With stagnant sales, Stellantis already announced a pivot away from earlier plans of turning Wagoneer into a luxury spinoff. Simply put, the market is ripe for price negotiations on this model. Even with major discounts, are you willing to spend $100,000 on a Jeep? Believe it or not, that’s about how much these luxury Jeeps cost.

The Nissan Titan, with its price hiked by $5,000 for the 2024 model year, contrasts starkly against its modest sales figures, selling just 19,189 units in 2023. This lack of market traction, especially compared to giants like Ford’s F-Series, suggests that the Titan could see significant price negotiations or cuts to align with its market performance, making it an attractive option for truck buyers looking for value.

If Nissan truly wants to grab truck market share, they’re going to have to work for it with aggressive pricing. Don’t pay a dollar over MSRP for a new Titan in 2024.

Performance-wise, the Solterra just isn’t worth the high price tag. But I may change my thinking if Subaru takes cues from the sluggish market and drops prices by $5,000. The Subaru Solterra, already experiencing price cuts in Australia, faces slow sales in North America and even slower charging speeds.

Its strengths? High ground clearance and futuristic Subaru looks are two that come to mind. With sales failing to take off more than 18 months after launch and plenty of 2023 Solterras STILL sitting on the lot, it’s past time for a big price cut for this EV.

Volvo’s EV sales have yet to take off. With stiff competition from the likes of Tesla, the German luxury brands, and even Hyundai Motor Group, it’s not clear that they ever will. The C40 isn’t a bad car by any measure. It’s luxurious, great for urban tight spaces, and can go 297 miles on a charge.

But the price is a bit higher than many similar offerings in today’s market. Today, there’s a 425-day supply of Volvo C40s. That’s 8x the typical market average. Will Volvo take cues from today’s EV buyers and lower prices? We hope so.

While these six models have not yet seen the price cuts that other vehicles have in 2024, their high inventory and slow sales make them prime candidates for negotiation. Keeping an eye on these models could lead to significant savings, but only if you’re patient.

Even before OEMs announce revised pricing, these six models are highly negotiable, especially if you are equipped with these insights and local market data. Don’t forget that we have not one, not two, but SEVEN free car buying cheat sheets available for download. Get your free resources here.

The good news is that some automakers are already making moves and lowering prices.

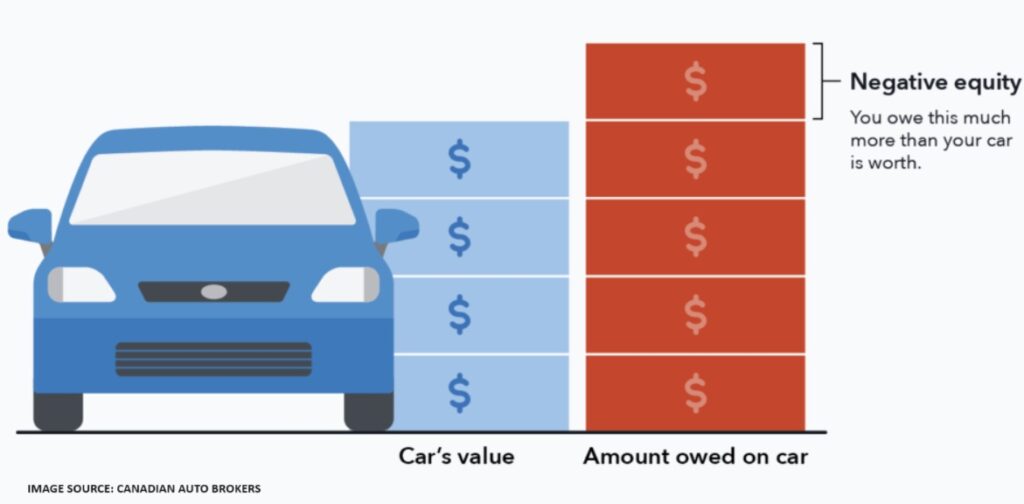

Diving into the world of car ownership can lead you into murky waters, especially when grappling with negative car equity. Imagine owing more on your car loan than the vehicle is worth – a situation many Americans face today. This comprehensive guide illuminates the shadowy depths of negative equity: exploring its causes, the impact of recent economic trends, and, most importantly, effective strategies to steer clear of or manage it if you’re already caught in its grip.

Understanding Negative Equity: How It Happens

Negative equity, often described as being “upside-down” on a car loan, occurs when the loan balance surpasses the vehicle’s current market value. This financial quagmire can ensnare car owners due to:

Depreciation: Cars depreciate the moment they’re driven off the lot. If the loan repayment lags behind this depreciation rate, negative equity can develop.

Long-term Loans: Extending loan periods results in slower principal repayment, risking negative equity as cars depreciate faster than the loan diminishes.

Small Down Payments: Minimal initial down payments increase the financed amount, heightening negative equity risks if the car’s value rapidly decreases.

Rolling Over Loans: Incorporating remaining debt from a previous car into a new loan can immediately create negative equity.

Understanding these factors is key to avoiding or mitigating negative equity and ensuring a financially stable ownership experience.

The Rise of Negative Equity in Car Loans

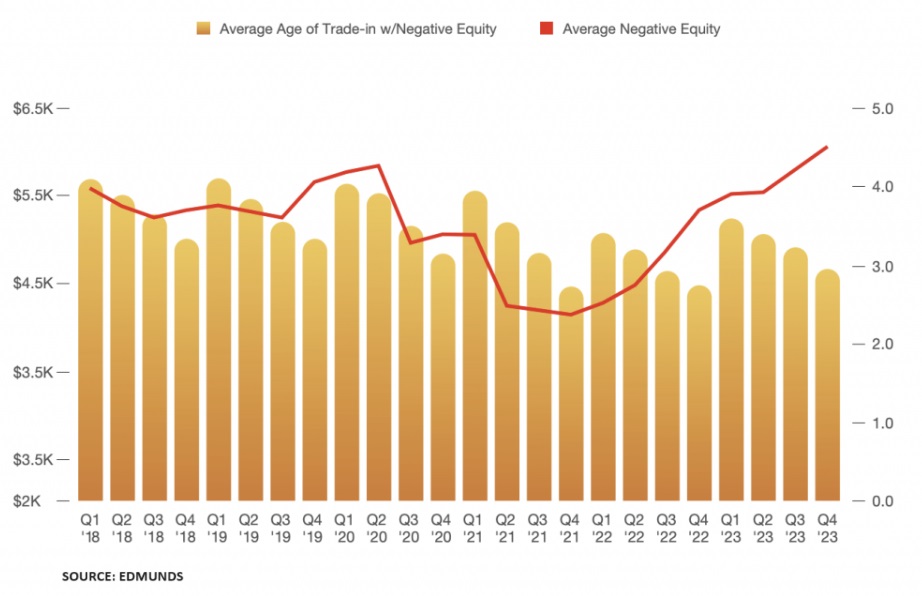

The phenomenon of negative car equity has been escalating, with recent Edmunds data revealing that 1 in 5 trade-ins have negative equity. The situation has become particularly pronounced in the new car market, where 20.4% of trade-ins are underwater, marking a significant jump from 14.9% in Q4 of 2021.

The average negative equity on car loans has surged to $6,054, setting a new record. This increase is partly attributed to the economic fluctuations during the pandemic when many consumers purchased vehicles at higher prices, leading to loans that exceeded the depreciating value of their cars. Consequently, drivers who bought cars during the pandemic are now facing the brunt of this financial imbalance.

What Negative Equity Means For You

Having negative equity on a car loan is more than just a numerical imbalance. It’s a predicament that can have lasting financial repercussions. Negative equity limits the owner’s flexibility, complicating efforts to sell or trade in the car without incurring losses.

For those looking to buy a new vehicle, negative equity means that the debt from the current car can roll over into the new loan. This leads to a cycle of increased debt that never seems to go away. Moreover, negative equity can affect credit scores and future loan conditions.

To combat these implications, car buyers should prioritize loan repayment strategies that target the principal amount. Also, consider shorter loan terms to align with the depreciation of the vehicle, and stay informed about the car’s current market value to make timely financial decisions. If you’d rather avoid the risk altogether, leasing is also an option.

Tackling Negative Equity

Navigating out of negative equity requires a proactive and strategic approach. Here are comprehensive steps and solutions to help you manage or eliminate negative car equity:

Accelerate Loan Repayment: One of the most straightforward methods to reduce negative equity is to make additional payments towards the loan’s principal. This will decrease the loan balance faster than the standard amortization schedule.

Refinancing the Loan: If you have good credit and interest rates have dropped since you took out your original loan, refinancing can be a smart option.

Consider a Shorter Loan Term: When refinancing, opting for a shorter loan term can result in higher monthly payments but will significantly reduce the interest cost and speed up equity building.

Lease a New Car: If you’re frequently facing negative equity with purchased vehicles, leasing might be a better option. Leasing a car can provide predictable monthly payments and eliminate the risk of negative equity, as you return the vehicle at the end of the lease term.

Cash-Injection on Trade-In: When looking to trade in a vehicle with negative equity, consider making a cash payment to cover the gap between the vehicle’s value and the loan balance. This can prevent the negative equity from rolling into the new loan.

Stay Informed About Your Car’s Value: Regularly check your vehicle’s current market value using tools like Sell With CarEdge, where you can receive multiple online offers at once. This awareness can help you make informed decisions about when to sell or trade-in the vehicle before the negative equity grows too large.

By employing these strategies, you can tackle negative equity head-on and work towards a more stable financial situation with your vehicle. Each approach has its considerations, so it’s important to evaluate your financial circumstances and car value carefully before deciding on the best course of action.

GAP (Guaranteed Asset Protection) insurance is indeed related to the topic of negative equity in car loans. Thus kind of insurance is designed to cover the difference between the actual cash value of a vehicle and the balance still owed on the financing (loan or lease) in the event that the car is totaled or stolen. Here’s how it connects to negative equity:

Protection Against Negative Equity: If a car is totaled or stolen, standard auto insurance policies usually cover only the current market value of the vehicle. If you owe more on your loan than the car is worth (negative equity), you would have to pay the difference out of pocket. GAP insurance covers this “gap,” preventing the financial strain of paying off a loan for a car you no longer possess.

Financial Safety Net: For car owners who are in negative equity, GAP insurance acts as a safety net, ensuring that they are not financially burdened by the remaining loan balance in case of total loss or theft of the vehicle.

Recommended for Long-Term Loans and Small Down Payments: For those who finance with long-term loans or small down payments, it’s smart to consider GAP insurance. It’s especially wise for leases and loans where the term extends beyond the standard three to four years.

In the context of managing negative equity, GAP insurance doesn’t reduce the loan balance or directly help in getting out of negative equity. However, it provides financial protection against the consequences of having negative equity in the event of an accident or theft.

Negative car equity, while daunting, is manageable with smart decisions and strategic actions. Understanding its roots and applying tailored strategies can lead car owners from the depths of financial strain to the clearer waters of financial stability and equity.

Want to learn more about how your particular situation may impact your ability to buy or sell? Chat with a CarEdge expert today. We’re here to help!

Electric vehicles are in the news for all the wrong reasons these days. Automakers are losing money as the clock ticks towards electrification goals set by the US government. Ford, who has struggled selling EVs to its core following, has gone so far as to cut two-thirds of the workforce at the Rouge Electric Vehicle Center in Dearborn, Michigan. But there’s good news, if you look beyond the headlines. Price cuts have come in waves, sending Ford’s EV prices falling. Ford’s EVs now have access to the Tesla Supercharger network, essentially fixing previous charging woes overnight. New numbers from CarEdge Data reveal that something is working, and Ford is selling EVs in higher numbers than ever before.

Here’s a closer look at Ford’s EV sales turnaround.

Ford’s EV Sales Are Up 114%

Over the course of March, Ford’s electric vehicle sales rates jumped 114%, as measured by running 45-day sales totals. For Ford, this is an unprecedented spike in EV sales.

For Ford’s first flagship EV, the Mustang Mach-E, sales rates are up 179% in just 30 days. In the 45 days leading up to March 1, 2024, 2,096 Mustang Mach-Es were sold in America. By March 30, the running total had climbed to 5,868 sold. This uptick in sales brough the Mustang Mach-Es market day supply down from 510 days at the start of March, to 137 days by the end of the month.

The best-selling electric truck in America, the F-150 Lightning, also saw sales rise last month. The Lightning’s 45-day running sales total climbed from 2,193 sales leading up to March 1, all the way to 3,334 sales by the end of the month. Ford’s electric truck sales jumped 52% in just three weeks.

For both models, nearly all sales were for the remaining 2023 models. 2024 models are just now arriving on dealer lots, making up just 19% of Ford’s EV lot inventory on April 1.

Who to Thank: Lower Prices, Or Tesla Superchargers?

Who is Ford to thank for their accelerating EV sales, their pricing strategy, or Tesla? Perhaps it’s a little bit of both.

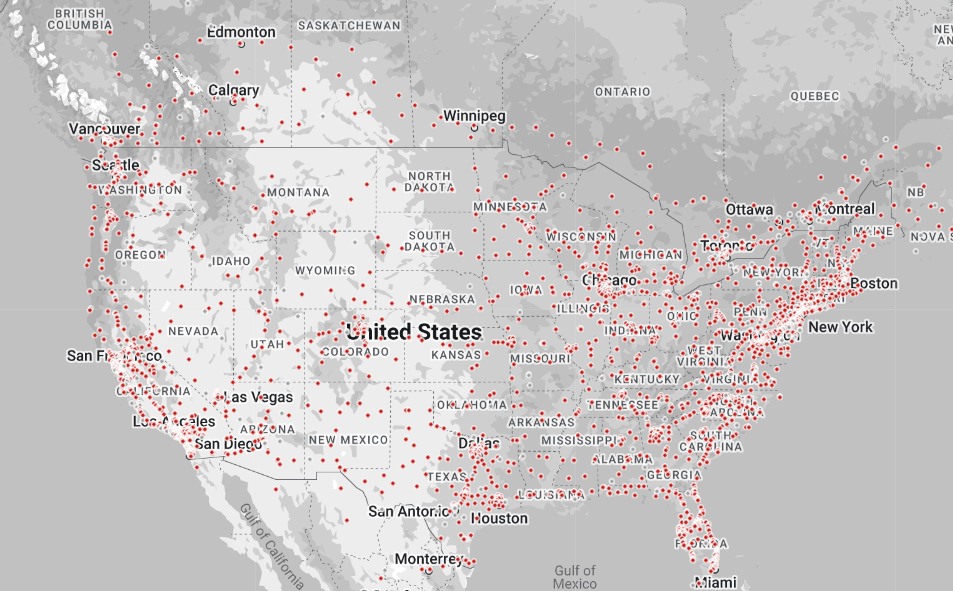

On February 29, Ford announced that all of its EV owners have access to Tesla’s Supercharger network. To the uninitiated, this may not sound like much news at all. But for any non-Tesla EV driver (like myself), it’s a big deal. Tesla may have its faults, but one of its many strengths is its charging network. Frankly, most other charging networks are horrible. Until now, the Tesla Supercharger network has been reserved for Tesla drivers only. Now, first with Ford and then with Rivian, Tesla is opening up access to other automakers.

Here’s a look at the current extent of the Tesla Supercharger network in 2024:

At last, reliable EV charging has arrived for Ford’s customers (as long as they have an adaptor, provided free of charge by Ford). But there’s more to this story than easy charging.

Just how far have Ford’s EV prices fallen recently?

As of April 1, the average selling price for a new Ford Mustang Mach-E is $52,927. At the start of 2024, the Mustang Mach-E’s average transaction price was $56,546. That’s a 6.4% price drop, all within a few months.

For the F-150 Lightning, average transaction prices fell from $71,118 at the beginning of 2024 to $66,391 by the end of the first quarter. That is also a 6.4% drop over three months.

Ford’s used EV prices have taken quite the tumble, too. Used F-150 Lightning prices are down 13.8%, and the Mustang Mach-E’s average used sale prices are down 10.5% in the first quarter of 2024.

Taking EVs Seriously Pays Off For Ford

EV skeptics repeat two major obstacles that keep them hesitant to make the switch: access to reliable charging, and high prices. In the span of a month, Ford has addressed both of these pain points. This is great news for EV buyers, and also something that Ford is surely happy to see.

Will the good news continue for Ford? It’s far too soon to tell. The remainder of 2024 will prove to be a make-or-break time for not only Ford, but all electric vehicle makers. But it’s safe to say that lower prices and better charging are two big steps in the right direction.

Want to do your own local market research? CarEdge Data is for you.

Welcome to your go-to guide for March’s end-of-month car specials. Learn the art of deal hunting with free resources like cheat sheets and strategy cards, and deepen your knowledge with our free Deal School course. We’ll also share the top 5 car deals right now. With the quarter ending and market dynamics in play, now is a prime time to find your perfect car and save A LOT of money. Let us help you navigate the deals and drive home happy.

The Best Tools For Deal Hunters

At CarEdge, we want to help ALL car buyers save money and avoid the hassle that usually comes with car buying. Core to that goal is providing both free and premium resources for all. As you head out to find the best car deals, we want to equip you with these tools.

You won’t find these anywhere else!

CarEdge Free Resources

Car Buying Cheat Sheets: Download 7 PDFs to help you level the playing field. Topics include a general car buying cheat sheet, negotiation guides, leasing guides, and our guide for first-time car buyers. Get your 100% free downloads here.

The Best Car Deals, All in One Spot: We’re deal hunters ourselves, so we’re always tracking the latest new car deals. These are your go-to pages, save them to your bookmarks! All of these are updated monthly:

Free Data: For any new or used car, see cost of ownership data, maintenance cost data, insurance costs, and more. Here’s your jumping off point.

Deal School: Want to learn from Ray and Zach? Master negotiation and learn the difference between a good deal and a bad one with our 100% free course, Deal School. Sign up and track your progress today.

Powerful Premium Resources

If you’re interested in taking your car buying skills AND savings to the next level, we have options for every budget…

Looking for advanced behind-the-scenes insights?Try CarEdge Data. See local price and inventory metrics that typically only the dealers have. It’s empowered car buying for all!

Not sure if you’re getting a good deal? Chat with a CarEdge Coach! We have options to fit every budget. Learn more about how we can help.

The Best Car Deals This Month

Remaining 2023 Ford F-150s

The Best Offer: Salem Ford in New Hampshire has remaining 2023 F-150s discounted between $2,450 and $4,900 off of MSRP. This is BEFORE any rebates or incentives. Free shipping is available within 700 miles.

Better yet, Ford is offering 1.9% APR for 72 months, plus NO payments for 90 days.

The Best Offer: Key Hyundai is discounting their 4 remaining 2023 Santa Fe’s by $3,400 to $4,500 off of MSRP. Free shipping is available within 700 miles.

On top of the MSRP discount, Hyundai is offering 0% APR for remaining 2023 Santa Fe Hybrids.

The Best Offer: Ford is offering huge discounts and incentives on the Mustang Mach-E electric crossover. Reviewers love it, but the previously high price kept many customers away. Now, it’s more affordable than ever.

Cash Discount: 0% APR for 72 months + $3,000 off MSRP + No payments for 90 days

The Best Offers: Right Now, Mazda is offering 0% APR for 36 months for the 2024 CX-50 and 2024 CX-30. Also, the 2024 CX-5 is available for 0.9% APR. With the average new car loan rate near 10% APR right now, these deals could save you thousands of dollars over the life of your loan. We have pre-negotiated prices secured to take the hassle out of buying your Mazda.

See these listings (with FREE home delivery available in select regions)

2024 Toyota RAV4

The Best Offer: $1,000 below MSRP for 2024 Toyota RAV4s. This is one of the best deals we’ve negotiated through our CarEdge Network of dealers. After all, the RAV4 is the best-selling crossover in America!

FREE home delivery is available in select regions.

The end of March is also the end of the quarter for automakers and car dealers. That means they’re particularly eager to sell cars at a discount to boost their numbers. Plus, with the Baltimore Bridge collapse threatening the auto industry, now is the time to buy for drivers who are in need of a car.

However, if you’re in no rush to drive home a new set of wheels, the end of the year is almost always the all-around best time of the year to buy. Waiting for year-end deals is always a good idea for those who can.

States eligibile for below invoice pricing and 100% free delivery:

Alabama, Arkansas, Texas, Oklahoma, Florida, Georgia, Kentucky, Louisiana, Maryland, Delaware, Mississippi, North Carolina, South Carolina, Tennessee, Virginia, and West Virginia.

What if I don’t live in these states? If you're outside these areas, don't worry! We're committed to making sure everyone can enjoy our deals. Although the delivery fee will not be waived, you can still purchase from CarEdge and either pay for shipping or coordinate pickup at a participating dealer.

Getting Started!

Please enter the following information to generate a price-transparent price quote.

FAQ

How much does it cost?

Our concierge service costs $999 plus an optional shipping fee (based on distance or pick-up).

To get started, pay the one-time payment of $999 and a CarEdge concierge will start by negotiating the vehicles in your favorites.

Why should you let a concierge do the work?

Get the best deal

Our team of concierges and industry experts with 75+ years of combined experience with access to tools and data to leverage the best deal possible.

Convenience

Gone are the days of looking for a car and stepping into the dealership spending hours and hours of head banging only to get smooth talked into a higher price.

Expert assistance

We answer all questions you may have regarding the buying process, what the right car is, the deal itself, and more!

Who are the concierges?

Transparent when others aren't

Our commitment to transparency and honesty ensures that you make informed decisions, while our years of experience guarantee that we will be able to secure the best deal for you.

When you win, we win

We work for you, not the dealership, ensuring your interests are always our top priority.

Buying a car just got a whole lot easier.

What happens next?

We’ll coach you on how to get dealers competing to get the best price

You’ll get instant access to our car buying checklists, guides, and market insights

What’s included in my car buying toolkit?

Dealer Invoice Price

Access the Dealer’s Invoice Price to negotiate an even better car deal.

Target Discount

A recommendation of for how much you should negotiate towards.

Negotiation Guide

Know exactly what you need to say to dealers to secure the best deal.

Exclusive Data

Info about your car such as cost of ownership, sales data, and more!