Get access to the same vehicle valuation tool that dealers rely on. With Black Book, you’ll have insider data to accurately assess trade-in and purchase values—empowering you to negotiate the best possible deal.

Year-end car deals aren’t just for new cars and trucks – smart shoppers in the used car market can leverage new car specials for big savings. Used car prices have been steadily declining, and the timing couldn’t be better to secure a great deal. Here’s how to use market trends and negotiation tools to your advantage this December.

Why Now Is the Time to Shop for a Used Car

Year-end car buying season is well-known for flashy new car promotions, but the holidays also create opportunities for used car buyers. With dozens of 0% APR financing offers and competitive lease deals pulling buyers to new car lots, demand for used vehicles has softened.

For used car buyers, that means one thing: leverage.

However, new car offers are so great that it’s totally reasonable for many would-be used car buyers to check them out first:

Still set on negotiating the best used car deal this month? Let’s take a look at how to bring your own car buying toolkit with you to lock in big savings. With the right tools and negotiation know-how, you’ll confidently drive home a deal you can be proud of.

Key Negotiation Tools to Bring to the Dealership

1. A Pre-Approval Letter for Competitive Financing

Arrive at the dealership armed with a pre-approval letter from a credit union, bank, or online lender. Not only does this save you time at the dealership, but it also provides leverage if the dealership’s financing offers can’t match or beat your pre-approved rate. Credit unions often have the best rates for used car buyers.

2. Black Book Value for the VIN You’re Interested In

Knowledge is power in any negotiation, and knowing the true value of the car you’re eyeing is key. Black Book, the valuation tool used by dealerships, provides real-time data on what a vehicle is worth. Before heading to the lot, check the Black Book value for the specific VIN to ensure the asking price is fair—or to use as leverage if it’s not. Access unlimited Black Book valuations with CarEdge Insights.

3. Days on the Lot, and Other Market Data

Dealerships want to move older inventory, and vehicles that have been sitting on the lot for a long time are prime for negotiation. Use CarEdge Insights to find out how long the car has been on the lot. If it’s been sitting for 60 days or more, you have a better chance of negotiating a lower price.

Some used cars have been on the lot for 6 months or longer, and are HIGHLY negotiable. However, don’t expect the car salesperson to volunteer this information!

4. Free Car Buying Cheat Sheets

A car buying cheat sheet is your go-to guide for navigating the deal. Know what’s fair, identify unnecessary add-ons to avoid, and recognize when it’s time to walk away from a deal. The more informed you are, the less likely you are to overpay. Download your negotiation cheat sheets, and take them with you to the dealership!

More Tips for Year-End Used Car Buying

Shop at the End of the Month: Dealers are eager to hit sales targets and clear inventory before the new year, making them more likely to agree to lower prices or added perks during the last days of December.

Compare Prices Online: Don’t settle for the first deal you see. Browse local inventory online to see which dealers are pricing competitively and which cars are sitting longer than others.

Get a Pre-Purchase Inspection: It’s always worth the peace of mind to have an independent mechanic complete a pre-purchase inspection on any used vehicle you’re serious about. If the dealer is not okay with it, that’s a deal breaker.

Check for Recalls: Before signing the dotted line, verify that the car hasn’t been affected by any recalls. If it has, confirm that the necessary repairs have been made.

Be Ready to Walk Away: Your greatest strength as a buyer is your willingness to leave if the deal isn’t right. Dealers are more likely to work with you when they know you’re not desperate to buy.

As the year comes to a close, the combination of falling used car prices and lower demand creates the perfect storm for savings. By coming prepared with the tools and insights you need, you’ll have everything you need to negotiate the best possible deal.

For more real-time market insights and negotiation tools, learn more about CarEdge Insights (25% off!). With CarEdge by your side, you’re sure to drive home the car you want—at the price you deserve.

Congratulations! You’ve just bought a new car—paperwork signed, plates in the mail, and the open road ahead. Now, you’re wondering: do you really need a warranty for your brand-new ride? After all, isn’t it built to last?

Auto warranties can feel like a gamble. If you don’t need it, it seems like an unnecessary expense. But if you do, not having one can set you back thousands of dollars. For new car buyers, the decision is often clearer than you might think.

The purpose of a warranty is simple: pay a little now to potentially save a lot later. When purchased at the time of buying a vehicle, warranties typically come with the best rates and most comprehensive coverage. Let’s dive into why a warranty might be worth it for new car owners, especially those looking to keep their vehicles for years to come.

Why Warranties Matter for New Cars

Although it’s rare for a brand-new car to break down in its first year, time and mileage take their toll. Road conditions, driving habits, and even weather can put significant strain on your car’s components. As your car ages, the likelihood of breakdowns increases—and so does the cost of warranty coverage.

Buying a warranty at the time of purchase locks in lower rates because warranty providers view new car buyers as lower-risk customers. This is particularly valuable if you plan to keep your car for a long time. Waiting to purchase coverage years down the road will almost certainly mean higher costs for less favorable terms.

The True Cost of Waiting

Let’s compare Fred and George, two Toyota Corolla owners.

Fred’s Story: Fred just bought a 2025 Corolla with 100 miles on it. He opts for an extended warranty through CarEdge and secures eight years and 150,000 miles of coverage for $2,234. Driving 18,750 miles annually, Fred feels confident knowing he’s protected through the life of his car.

George’s Story: George bought his 2021 Corolla brand new but waited to explore warranty options until now, after four years and 75,000 miles. He looks for the same 150,000-mile total coverage but only needs four additional years. His quote? $3,445—55% more expensive than Fred’s, for half the coverage.

This example highlights a key benefit of buying a warranty early: locking in the best pricing and terms available. For drivers planning to keep their vehicles long-term, this decision can save thousands.

CarEdge + Fair: Comprehensive Coverage You Can Trust

At CarEdge, we’re committed to helping drivers save money and protect their investments. That’s why we’ve partnered with Fair, a trusted provider of extended warranties designed with drivers in mind.

With Fair’s extended warranties, perks like roadside assistance, fuel delivery, trip interruption coverage, and rental car reimbursement come standard. Fair guarantees transparency at every step, from their easy-to-navigate claims portal to a straightforward cancellation and refund process.

Here’s what sets Fair apart: they cover repairs up to the value of your vehicle. Unlike many warranty providers that cap coverage for major repairs, Fair ensures drivers get the protection they need without hidden limitations.

Peace of Mind for the Road Ahead

A warranty isn’t just about saving money—it’s about providing long-term peace of mind. By purchasing coverage when your car is new, you secure the best rates, the most comprehensive protection, and the confidence that your vehicle is ready for whatever comes its way.

With CarEdge and Fair, you’ll find coverage you can count on. Start protecting your investment today and drive with peace of mind knowing you’re covered.

Negative equity, or owing more on a car loan than the vehicle’s market value, continues to rise as inflationary pressures and long loan terms take their toll on car buyers. CarEdge, in partnership with Black Book, surveyed 474 drivers in Q4 2024 to uncover the state of vehicle equity. Here are the highlights and the broader implications for drivers, car buyers, and the automotive industry.

In Q4 2024, 39% of drivers who financed their vehicles were underwater—up from 31% in Q3, a 25% jump. For cars purchased since 2022, the situation is even worse: 44% of these buyers owe more than their car is worth. As depreciation accelerates and long-term loans become the norm, the risk of negative equity continues to grow. This trend highlights a troubling financial burden on drivers and poses risks for the broader auto market.

Drivers Overestimate Their Car’s Value

Our survey reveals that 60% of drivers believe their car is worth more than its actual trade-in value. Of these, 18% overestimate by $5,000 or more, and 7% by over $10,000. This disconnect leads many to carry negative equity into their next car purchase, perpetuating financial strain.

When drivers attempt to trade in or sell their vehicles, they often face the harsh reality of lower-than-expected offers, which can derail their car-buying plans. Unfortunately, many choose to roll over the remaining debt into their next loan. This practice, while common, leads to higher monthly payments and extended loan terms, keeping buyers in a cycle of financial vulnerability.

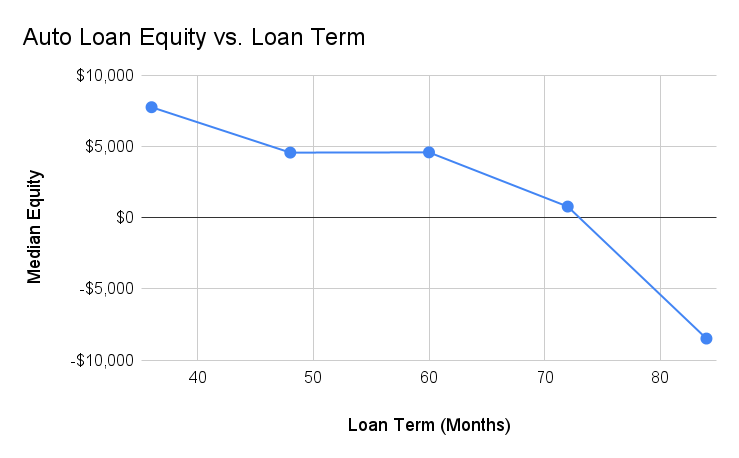

Long Loan Terms Drive Negative Equity

Loan terms significantly impact vehicle equity. Borrowers with 84-month loans face a median negative equity of -$8,485, while those with shorter 36-month terms have a positive median equity of $7,783. While longer loans make monthly payments more affordable, they also leave buyers trapped in equity-negative positions for years.

For many buyers, the appeal of lower monthly payments outweighs the long-term risks. However, as loan balances decrease more slowly with longer terms, these borrowers are more likely to face financial strain when attempting to sell or trade in their vehicles. Buyers who opt for shorter terms and make larger down payments tend to build equity more quickly, putting them in stronger financial positions.

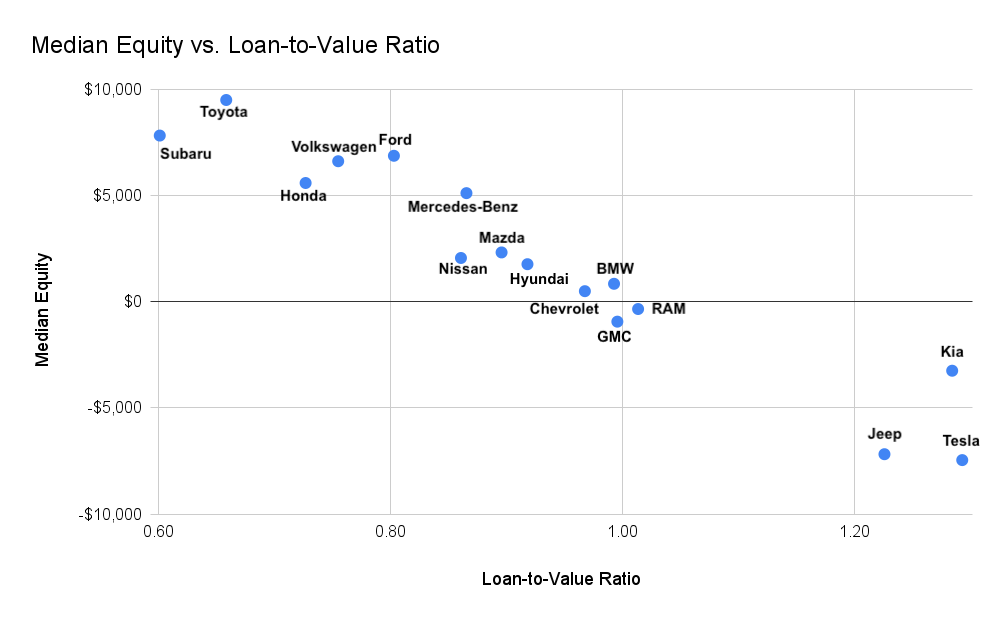

EV Owners Are Most at Risk

Electric vehicle owners face the highest negative equity rates, with 54% underwater and a median equity of -$2,345. This makes EVs particularly vulnerable compared to gas and hybrid vehicles, which are more likely to have positive equity.

The rapid depreciation of EVs is a key driver of this trend. EV technology can become outdated quickly as newer models with improved range, charging speeds, and driver assistance features enter the market. Additionally, concerns about costly battery replacements and limited resale demand have led many buyers to prefer new EVs with warranties and a known history, further impacting the resale value of used EVs.

For EV buyers, understanding depreciation trends and factoring in long-term costs is critical to avoiding significant negative equity. Opting for shorter loan terms and considering potential incentives or tax credits can help offset some of the financial risks. Buyers who plan to hold on to their EVs for longer than just a few years are less likely to be impacted by negative equity with their auto loans.

What Does This Mean for 2025?

As we head into 2025, the issue of negative equity looms large for both consumers and the auto industry. For car buyers, rolling over negative equity into new loans can lead to long-term financial stress, reducing their purchasing power and limiting options. For the auto industry, high levels of negative equity could dampen trade-ins and slow new car sales, forcing automakers and dealerships to adjust their strategies.

Car dealers also face challenges when appraising trade-ins with negative equity. To close deals, dealers may need to discount new vehicles more aggressively or offer creative financing solutions, which can erode profit margins. Over time, high levels of negative equity in the market can disrupt the typical sales cycle

Navigating the Negative Equity Challenge

The Q4 2024 Negative Equity Report paints a clear picture of a growing issue in the car market. Drivers, car buyers, and the auto industry alike must address the challenges posed by rising negative equity.

CarEdge remains committed to empowering consumers with tools and insights to navigate today’s challenging car market. To avoid falling into the negative equity trap, car buyers should prioritize shorter loan terms, be familiar with expected car depreciation, and monitor used car values with tools like Black Book. Overcoming negative equity is possible when drivers make informed car buying and ownership decisions.

Two of Japan’s largest automakers, Honda and Nissan, are reportedly entering merger negotiations, as reported by the Nikkei newspaper. The talks aim to solidify their position in the rapidly changing global automotive market, where rising competition, high production costs, and the EV transition are reshaping the industry.

The potential merger would create a holding company for Honda, Nissan, and Mitsubishi Motors, of which Nissan already holds a 24% stake. Combined, these automakers would account for over 8 million vehicle sales annually—enough to challenge global giants like Toyota (11.2 million vehicles sold in 2023) and Volkswagen (9.2 million vehicles sold last year).

For now, both automakers have neither confirmed nor denied the report. Honda stated: “The reported content was not released by our company… We will inform our stakeholders of any updates at an appropriate time.” This cautious tone reflects the sensitive nature of the negotiations, but one thing is clear: if this merger proceeds, it will mark one of the largest shakeups in the auto industry since Fiat Chrysler merged with PSA Groupe to form Stellantis in 2021.

Nissan’s Dire Situation

While Honda enters these talks from a position of strength, Nissan’s struggles have been front and center. Earlier this year, Nissan reported a 99% drop in operating profits in the North American market. The automaker’s woes stem from:

Higher Prices: Sticker shock has pushed buyers toward competitors.

Falling Reliability: Consumer trust has waned in key models.

Tough Competition: Toyota, Hyundai, and Kia continue to dominate Nissan’s segments.

Adding to the urgency, Nissan reportedly has just 12 to 14 months of cash reserves left. To stay afloat, Nissan has drastically increased incentives to lure buyers. Popular models like the Rogue, Altima, and Pathfinder are now offered with deals like 0% APR financingand cheap lease specials—a trend we expect to continue well into 2025.

Honda Stands Strong In contrast, Honda’s financial health remains robust. International sales are growing steadily, and U.S. demand for Honda models, like the CR-V and Civic, remains strong. Unlike Nissan, Honda hasn’t needed to lean heavily on incentives to maintain momentum.

What This Means For Car Buyers in 2025

The Honda-Nissan merger talks come at a crucial moment for car shoppers. Here’s what you need to know:

Expect Big Nissan Deals to Continue: Nissan’s financial troubles mean ongoing incentives like 0% APR, cash discounts, and cheap leases on remaining 2024 and incoming 2025 models.

Honda Pricing Will Remain Firm: Honda is holding strong. Don’t count on significant discounts unless the merger drastically shifts their strategy.

Mitsubishi’s Future Is Uncertain: If included in the merger, Mitsubishi could see sweeping changes, potentially phasing out less competitive models.

The automotive market is evolving fast, and buyers stand to benefit from brands under pressure. Nissan, in particular, will remain highly negotiable as it fights to stay competitive. Stay tuned to CarEdge News for up-to-the-minute insights on deals, trends, and automotive news that matter to you.

Car insurance premiums are surging at an unprecedented rate, and it’s hitting wallets hard. Over the past year, auto insurance costs have risen by 13%, following a nearly 51% increase since late 2019. According to a recent report from the Washington Post, this surge has become a major driver of overall inflation, complicating efforts to stabilize the economy. But why are car insurance rates climbing so sharply, and what can drivers do about it? Let’s break it down.

Why Are Car Insurance Rates Rising?

1. Expensive Repairs and Costly Cars

Car prices have been on the rise for years, with automakers prioritizing high-end models over budget-minded offerings. Today’s vehicles aren’t just more expensive; they’re also loaded with advanced driver assistance and safety features. While these features make vehicles safer, they also drive up repair costs. Replacing sensors, cameras, and other high-tech components is far pricier than traditional repairs that drivers are accustomed to. Additionally, labor costs in the auto repair industry have soared, further inflating the price of repairs that insurance companies must cover.

Distracted and reckless driving is leading to more accidents, injuries, and fatalities. According to data from the National Highway Traffic Safety Administration, distracted driving claims over 3,000 lives in the U.S. each year. Distracted driving results in more accidents, and as a result, more insurance claims. This uptick in claims drives up costs for insurance providers, who pass those expenses on to consumers. Attorney involvement in claims is also on the rise, adding to the rising costs of resolving insurance claims.

3. Uninsured Drivers Are Adding to the Problem

The rate of uninsured motorists has grown from 11.6% in 2019 to 14% in 2022, according to the Insurance Research Council. As more drivers go without insurance, insurers must spread the risk among their paying customers, driving premiums higher for everyone else.

According to data from ValuePenguin and Lending Tree, there are five states where more than 20% of drivers are uninsured: Mississippi (29%), Michigan (25%), Tennessee (24%), Florida (23%), and Washington (21%).

How Insurance Rates Are Impacting Inflation

Car insurance premiums are not just a personal financial burden—they’re influencing national economic trends. In November 2024, rising auto insurance costs accounted for 15% of the increase in overall consumer prices. Without the spike in premiums, inflation would have been significantly lower, according to economists cited by the Washington Post.

Federal Reserve Chair Jerome Powell has acknowledged that insurance costs are one of the “stickiest” contributors to lingering inflation, making it harder to achieve the Fed’s 2% inflation goal.

Will Car Insurance Rates Go Down?

There is some hope for relief. As auto prices stabilize, insurance premiums may follow. November’s CPI data showed only a 0.1% monthly increase in auto insurance costs, hinting at a potential plateau. However, economists warn that factors like potential tariffs on car parts from Canada and Mexico could reignite price hikes.

Additionally, as more drivers forgo insurance, premiums for insured drivers may remain elevated or even rise further. Without systemic changes, drivers should brace for a long road ahead when it comes to high insurance costs.

What Can Drivers Do to Save?

While systemic factors are driving insurance rates, there are steps you can take to lower your costs:

Bundle Policies: Combine home and auto insurance to access discounts. Before you switch insurance providers for a slightly lower rate, make sure that you wouldn’t be losing any bundling discounts.

Maintain a Clean Record: Avoid accidents and tickets, as they can significantly raise your premiums.

Consider Higher Deductibles: If you’re confident in your driving and live in a region with a low number of uninsured drivers, increasing your deductible could lower your monthly costs.

Reevaluate Coverage: For older vehicles, dropping comprehensive and collision coverage may save money. If you do this, it’s important to understand the risks of not having auto insurance, such as much higher repair costs in the event of an accident.

Stay Informed, Compare Quotes Often, and Stay Alert For Savings

Soaring car insurance premiums are putting a strain on household budgets and driving inflation higher. While there may be hope for auto insurance rates stabilizing in the future, drivers should take proactive steps to mitigate rising costs. Compare quotes from multiple insurers to see if you have the best rate. It’s free, and can’t hurt.

States eligibile for below invoice pricing and 100% free delivery:

Alabama, Arkansas, Texas, Oklahoma, Florida, Georgia, Kentucky, Louisiana, Maryland, Delaware, Mississippi, North Carolina, South Carolina, Tennessee, Virginia, and West Virginia.

What if I don’t live in these states? If you're outside these areas, don't worry! We're committed to making sure everyone can enjoy our deals. Although the delivery fee will not be waived, you can still purchase from CarEdge and either pay for shipping or coordinate pickup at a participating dealer.

Getting Started!

Please enter the following information to generate a price-transparent price quote.

FAQ

How much does it cost?

Our concierge service costs $999 plus an optional shipping fee (based on distance or pick-up).

To get started, pay the one-time payment of $999 and a CarEdge concierge will start by negotiating the vehicles in your favorites.

Why should you let a concierge do the work?

Get the best deal

Our team of concierges and industry experts with 75+ years of combined experience with access to tools and data to leverage the best deal possible.

Convenience

Gone are the days of looking for a car and stepping into the dealership spending hours and hours of head banging only to get smooth talked into a higher price.

Expert assistance

We answer all questions you may have regarding the buying process, what the right car is, the deal itself, and more!

Who are the concierges?

Transparent when others aren't

Our commitment to transparency and honesty ensures that you make informed decisions, while our years of experience guarantee that we will be able to secure the best deal for you.

When you win, we win

We work for you, not the dealership, ensuring your interests are always our top priority.

Buying a car just got a whole lot easier.

What happens next?

We’ll coach you on how to get dealers competing to get the best price

You’ll get instant access to our car buying checklists, guides, and market insights

What’s included in my car buying toolkit?

Dealer Invoice Price

Access the Dealer’s Invoice Price to negotiate an even better car deal.

Target Discount

A recommendation of for how much you should negotiate towards.

Negotiation Guide

Know exactly what you need to say to dealers to secure the best deal.

Exclusive Data

Info about your car such as cost of ownership, sales data, and more!